Retiring early is a dream for many, but for those with only $300,000 saved by age 55, that dream may seem just out of reach. Still, in 2025–2027, more Americans are exploring creative paths to financial independence — without hitting the classic $1 million target. The real question is: Can you retire at 55 with $300,000 and still live a secure, fulfilling life?

The answer depends on how you define retirement, how flexible your lifestyle is, and how you manage income, expenses, and risk. While $300,000 alone isn’t enough to fully retire in most parts of the U.S., it can be enough to launch an alternative retirement path — especially if you take advantage of Social Security later, lower-cost living options, and hybrid retirement models.

Let’s break down what’s possible and how to make the math work.

Understanding the Retirement Gap (55–62)

Retiring at 55 means you’re still seven years away from being eligible for Social Security (age 62 at the earliest) and ten years away from Medicare (age 65). That’s a crucial challenge: $300,000 has to cover all your living and healthcare costs in the meantime — without help from two of the biggest government support programs.

If you live on a tight budget of $30,000/year, you’ll need $210,000 just to bridge the seven-year gap. That leaves only $90,000 for the rest of your retirement — unless you supplement with income or reduce costs substantially.

That’s why most people who retire with $300K at 55 don’t stop working entirely. Instead, they pivot to semi-retirement, geoarbitrage, or slow drawdown strategies until their full benefits kick in.

Semi-Retirement: Easing Into Full Retirement

Many people with $300,000 in savings at age 55 adopt a semi-retired lifestyle rather than quitting work entirely. This could mean part-time work, freelancing, or turning a hobby into a modest income stream. Even earning $1,000 to $1,500 per month can significantly reduce the pressure on your savings and extend the lifespan of your retirement nest egg.

Here’s a sample hybrid retirement budget for a solo retiree living modestly:

| Category | Monthly Cost | Notes |

| Rent (low-cost area) | $700 | Could be lower abroad or in rural U.S. |

| Groceries | $300 | Basic healthy diet |

| Health Insurance (pre-65) | $500 | ACA marketplace or subsidized plan |

| Utilities & Internet | $200 | Modest home setup |

| Transportation | $150 | No car or very limited use |

| Entertainment & Other | $150 | Frugal lifestyle |

| Total | $2,000 | Target budget for lean semi-retirement |

With this plan, if you earn $1,200/month part-time, you’d only need to withdraw about $800/month (or $9,600/year) from savings. That allows $300,000 to stretch well over 20 years, giving your retirement plan much more breathing room.

Social Security Strategy: Timing Matters

One of the most powerful tools in early retirement is delaying Social Security to increase your monthly payout. Claiming at age 62 may be tempting, but waiting until 67 or even 70 can boost your benefits significantly.

For example:

- Estimated Social Security at 62: $1,100/month

- At full retirement age (67): $1,570/month

- At 70: $1,940/month

If you can cover your living expenses until 67 using part-time income or savings, the higher benefit provides a stronger long-term safety net, especially if you live into your 80s or 90s.

Geoarbitrage: Living Abroad on Less

Another viable route for early retirees with limited savings is relocating to lower-cost countries where $300,000 stretches further. Countries like Portugal, Mexico, Thailand, or Colombia offer lower rents, affordable healthcare, and a slower pace of life. Some expats report living well on $1,200–$1,800/month, including rent, food, insurance, and entertainment.

This strategy can:

- Delay the need to tap Social Security

- Reduce the pressure on your savings

- Improve quality of life (warmer climate, lower stress)

Be aware that moving abroad comes with legal, healthcare, and tax considerations — but many early retirees say the trade-offs are worth it.

Investment Strategy: Make Your $300K Work

A smart, low-risk investment strategy is critical. You can’t afford to gamble, but you do need some growth. A 60/40 mix of ETFs and bonds, for example, might return 4–5% on average annually, enough to sustain withdrawals of 3–3.5%/year over 30 years in a modest scenario.

Here’s a sample asset allocation:

| Investment Type | % Allocation | Role |

| Dividend ETFs | 40% | Passive income & growth |

| Bonds or bond funds | 30% | Stability & income |

| Cash/CDs | 15% | Liquidity & safety |

| Gold/REITs/Other | 15% | Diversification |

This mix is conservative but can help your portfolio last into your 80s or beyond, especially when combined with part-time work and later Social Security.

Phased Retirement Timeline: A Sample Path from 55 to 80+

Let’s map out what a realistic early retirement could look like for someone with $300,000 saved at age 55:

| Age Range | Key Activities | Income Sources | Goals |

| 55–62 | Semi-retire, work part-time, cut costs, possibly move to a lower-cost location (U.S. or abroad) | Part-time income + limited withdrawals (≤3%) | Stretch savings, avoid Social Security |

| 62–67 | Fully retire or continue part-time; delay Social Security if possible | Savings + smaller withdrawals + possibly annuity or rental income | Wait for full SS benefit |

| 67–70 | Begin drawing full Social Security benefits | Social Security + small withdrawals | Reduce drawdown on savings |

| 70+ | Secure, fully retired lifestyle | Social Security + residual savings | Stability & simplicity |

This “phased retirement” approach helps avoid depleting your savings too soon while maximizing Social Security benefits.

Pros and Cons of Retiring at 55 with $300K

✅ Pros:

- Possible with frugal lifestyle or geoarbitrage

- Semi-retirement allows flexibility and meaning

- Healthier early retirement years

- Strategic investing and part-time income can extend lifespan of funds

❌ Cons:

- Risk of outliving savings if no plan

- Health insurance is expensive before 65

- Relies on market performance, low inflation, and stable spending

- Lifestyle sacrifices may be required

Key Takeaways

- $300,000 is not enough to retire “fully” at 55 in the U.S. without other income, but with creativity and frugality, it can work.

- You’ll likely need to combine part-time work, Social Security timing, smart investing, and possibly relocation to make this scenario sustainable.

- The biggest threat is running out of money in your 70s or 80s, so planning for multiple phases of retirement is essential.

Separate Thoughts: It’s Not Just About the Money

Many people focus only on the numbers, but retirement success also depends on mindset, adaptability, and emotional well-being. Retiring early at 55 with $300K is challenging — but not impossible — for people willing to be flexible.

You’ll need to monitor your spending closely, keep an eye on inflation, and possibly downsize or work occasionally. But if you value time and freedom over luxury, this type of early retirement could give you decades of control over your life.

Additional Income Streams That Can Help

If you’re concerned about running out of money, the key is to diversify your income — even in retirement. Here are several additional sources to consider beyond savings and Social Security:

1. High-Yield Savings and CDs:

While interest rates may fluctuate, some high-yield savings accounts and Certificates of Deposit (CDs) now offer 4–5% returns annually. Keeping a portion of your money in these instruments provides safety and some passive income. For example, $50,000 in a 4.5% CD would yield $2,250/year — enough to cover utilities or basic healthcare costs.

2. Dividend-Paying Stocks or ETFs:

For those comfortable with modest risk, a portfolio of dividend-paying stocks or ETFs can generate regular income. Many funds yield 3–4% annually. With $150,000 invested, this could bring in $4,500–6,000 per year.

3. Real Estate or House Hacking:

Renting a room, converting a basement to a studio, or even managing a small Airbnb can provide reliable monthly cash. Retirees with a mortgage-free home can significantly reduce expenses and add income this way.

4. Annuities (with caution):

A fixed annuity can convert a lump sum into guaranteed monthly payments for life. But fees and terms vary widely, so only consider annuities from top-rated providers and after reviewing them with a fiduciary advisor.

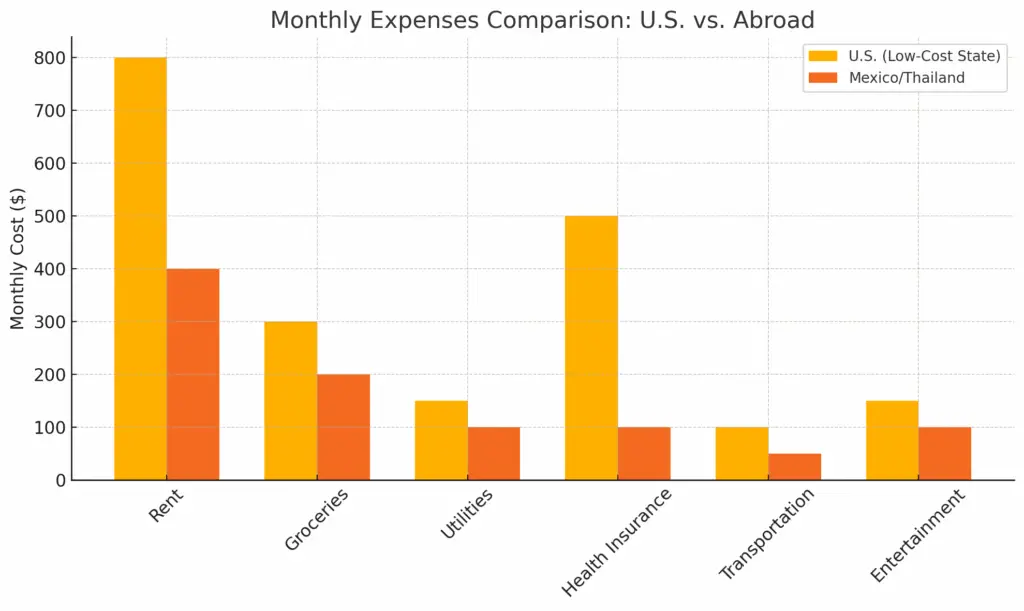

Sample Monthly Budgets (U.S. vs. Abroad)

Let’s compare what a frugal lifestyle might cost per month in the U.S. versus an affordable expat-friendly country:

| Category | U.S. (Low-Cost State) | Mexico/Thailand |

| Rent | $800 | $400 |

| Groceries | $300 | $200 |

| Utilities | $150 | $100 |

| Health Insurance | $500 | $100 |

| Transportation | $100 | $50 |

| Entertainment | $150 | $100 |

| Total | $2,000 | $950 |

In the U.S., you’d need at least $2,000/month, while in many countries abroad, $1,000/month covers essentials with room to spare. This makes relocation one of the strongest levers for stretching $300,000 over 20+ years.

Side Gigs That Don’t Feel Like “Work”

A lot of retirees want to stay active and mentally engaged — but without the pressure of a full-time job. Consider these:

- Tutoring online (math, English, or hobbies)

- Dog walking or pet sitting

- Writing articles, starting a blog, or self-publishing books

- Freelance consulting in your former profession

- Part-time retail or seasonal work (only a few months per year)

Even $500/month from a side gig cuts annual withdrawals by $6,000 — extending the life of your nest egg significantly.

Here is the comparison chart showing monthly expenses in a low-cost U.S. state versus typical costs in countries like Mexico or Thailand. This visual can help emphasize how much further your retirement budget can stretch abroad.

Maximizing Returns: Smart Investment Strategies for Early Retirees

While $300,000 may not seem like much for a 30-year retirement, the way you invest that money plays a crucial role in how long it lasts. Early retirees can’t afford to keep their entire portfolio in cash or low-yield savings accounts. Inflation will erode value over time — especially during the 2025–2027 period, where inflation remains a top concern globally.

A common approach is the “bucket strategy”, which divides your savings into three parts:

- Bucket 1: Cash & Near-Cash (for the next 1–2 years)

- Bucket 2: Bonds & Dividend Stocks (for 3–7 years)

- Bucket 3: Growth Investments (long-term growth, like stock index funds)

This strategy lets you weather downturns by not being forced to sell stocks when markets are down. You draw from cash first, then shift to more stable income, while the growth bucket continues compounding.

You can also consider:

- Roth IRA conversions during low-income years

- Annuities as supplemental income later in retirement

- Dividend ETFs that pay reliable monthly or quarterly income

Properly managed, even a modest portfolio can stretch further when paired with steady, low-risk returns.

The Importance of Flexible Spending

One of the secrets to early retirement is not rigid budgeting, but flexible spending. When markets are down or unexpected costs arise (like medical or home repairs), you need the flexibility to adjust — pause travel, downsize a rental, or take on light freelance work.

Those who succeed in early retirement are often the ones who treat spending as a range, not a fixed number. For instance:

| Market Year | Annual Spending |

| Strong Bull Year | $30,000 |

| Neutral/Flat Year | $25,000 |

| Recession Year | $18,000 |

This variable strategy helps protect your portfolio from being drained during downturns and lets you bounce back when things stabilize.

Emotional Readiness: Beyond the Financial Plan

Retiring early isn’t just a numbers game. Many retirees find that the emotional side of retirement is just as important — if not more.

When you retire at 55, you may lose:

- Daily structure

- Social connections from work

- A sense of identity tied to your career

That’s why it’s important to replace those missing pieces with meaningful activities. Whether it’s freelancing, volunteering, part-time teaching, travel, or learning new skills — retirees who stay active mentally and socially tend to report higher life satisfaction and better long-term health.

Start by asking:

- What will I do with my time?

- What purpose will I serve in this next chapter?

- Do I have a strong social network or plan to build one?

Answering these questions honestly can prevent depression, boredom, or regret after leaving full-time work.

Final Retirement Readiness Checklist

Before you decide to retire at 55 with $300,000, run through this checklist:

✅ Have I calculated my annual budget — including health care, housing, food, and travel?

✅ Do I have at least 1–2 years of liquid cash for emergencies?

✅ Have I built a conservative investment plan (e.g., 2–3% withdrawal rate)?

✅ Have I considered geoarbitrage or relocation to reduce expenses?

✅ Can I access affordable health insurance before 65?

✅ Do I have a plan for staying engaged and connected?

✅ Have I factored in Social Security timing and long-term care planning?

If most of these boxes are checked, you’re already ahead of many retirees.

Conclusion: Retiring at 55 With $300,000 — A Realistic but Careful Path

While retiring at 55 with $300,000 isn’t luxurious, it’s absolutely possible for people willing to live modestly, relocate, work part-time, or make creative lifestyle adjustments. It’s not a one-size-fits-all plan — but it’s one that more people are considering in 2025 and beyond as the nature of work and retirement continues to change.

The key isn’t just money — it’s strategy, flexibility, and vision. If you’re thoughtful and honest about your priorities, retiring at 55 on a lean budget can be one of the most freeing and empowering moves of your life.