How to Protect Your Savings Against Inflation and Market Volatility

In a world where markets swing wildly and inflation silently erodes purchasing power, millions of people are asking: is cash still safe in 2025 and 2026? Or better yet — is cash still king?

For decades, the traditional wisdom was simple: save money, hold some in cash, and sleep well knowing your capital is safe. But that old-school formula has been turned upside down. The COVID-19 aftermath, record money printing, global wars, and unpredictable central bank policy have shaken trust in cash. In today’s economic climate, relying too heavily on paper money could mean watching your life savings slowly lose value — even if your bank account balance doesn’t budge.

In this article, we break down the true risks of holding cash in 2025, explore better ways to protect your savings, and highlight smarter ways to balance liquidity, growth, and safety.

What Happened to Cash in the 2020s?

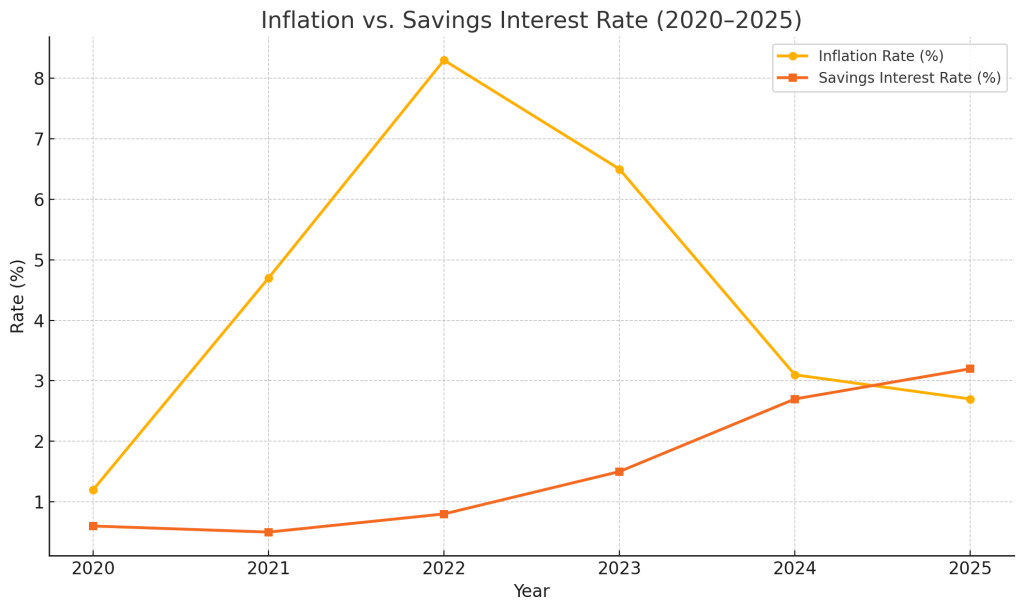

Cash used to be the ultimate symbol of safety. If you had dollars, euros, or pounds, you had freedom. But that changed after the 2020 global crisis. Central banks flooded the world with liquidity. Inflation spiked. Savings accounts offered interest rates far below inflation — sometimes even negative real yields.

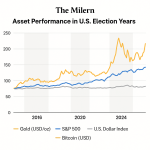

Fast-forward to 2025, and central banks have shifted to tightening, with interest rates at their highest in decades. But while rates may seem high on paper, inflation is still eating into real returns. A savings account offering 3.5% interest sounds nice, until you realize inflation is running at 4.2%. That means you’re still losing purchasing power every year — just more quietly. Read our article on why US dollar already collapsed, but you did not notice. Here is inflation and data chart from Federal Reserve.

Why Holding Cash in 2025 – 2026 Can Be Risky

While cash is useful and liquid, it’s not risk-free. In 2025, the biggest dangers include:

1. Silent Erosion from Inflation

Inflation remains sticky. Despite what policymakers promise, real inflation often outpaces official statistics. Food, rent, energy, and healthcare are more expensive than ever. That means cash held in savings is losing its ability to buy essentials.

2. Bank Instability Isn’t Over

While the panic of 2023-2024 regional bank failures has calmed, the structural weaknesses remain. Rising interest rates hurt bond-heavy portfolios at small and mid-size banks. If you’re parking large sums in a single institution, especially uninsured, you may be exposed.

3. Lost Opportunity Cost

With financial markets volatile but also full of opportunities, holding too much cash means missing out on potential gains from gold, Bitcoin, dividend stocks, or even inflation-protected treasuries (TIPS).

When Does Holding Cash Make Sense?

To be clear — holding some cash is essential. The key is how much, and why.

Here’s when cash is still smart in 2025 – 2026:

- 🛑 Emergency Fund: A 3–6 month cushion for unexpected bills or job loss

- ⏳ Waiting for Better Entry Points: Holding cash while waiting to enter volatile assets like crypto or tech stocks

- 🧘 Mental Clarity: During chaotic times, cash can help you stay calm and avoid panic selling

- 📉 Hedging Volatility: If you expect major short-term market dips, cash is a defensive shield

The danger comes when you stay in cash too long, especially with zero strategy for protecting its value.

Top Alternatives to Cash in 2025 – 2026

If you’re sitting on a pile of cash and feel stuck, it’s time to explore alternatives that offer both liquidity and protection. In this crypto-driven, inflation-haunted world, here’s what smart investors are considering:

1. High-Yield Savings & Money Market Funds

These offer slightly better rates than traditional accounts, sometimes above 4–5%, depending on the bank or platform. Still, in real terms, they barely keep up with inflation.

2. Short-Term Treasury Bills

U.S. T-bills are backed by the government and can offer 4–5% yields. You can buy them directly or through ETFs. They’re a safe, liquid alternative to cash — and better than a checking account.

3. Gold: The Timeless Hedge

Gold is up massively in recent years, hitting all-time highs in 2025. Why? Because investors are realizing fiat currencies are vulnerable. Gold doesn’t default. Gold doesn’t inflate. It may not pay interest, but it protects.

Gold-backed ETFs or even fractional gold accounts now make owning gold easier than ever. Read our Gold vs. Stocks 2025 article to understand how it compares in long-term strategy.

4. Bitcoin & Crypto Assets

Bitcoin remains volatile — but it has proven itself as a long-term hedge against fiat erosion. In 2025, BTC’s halving has already passed, and analysts are watching whether a new bull cycle is forming. While it shouldn’t replace your emergency fund, holding 1–5% in crypto is a strategy many modern investors are exploring.

How Much Cash Should You Really Hold in 2025 and 2026?

The million-dollar question isn’t whether cash is bad — it’s how much is too much?

The answer depends on your goals:

- 🧰 Emergency Fund: Everyone should hold 3–6 months’ worth of essential expenses in cash. This is your financial first-aid kit.

- 🎯 Short-Term Goals (0–6 months): Planning a large purchase? Keep that cash handy.

- 📉 Bear Market Patience: Traders and long-term investors often hold cash when they expect short-term dips.

But beyond that, cash becomes a drag. Every extra $1,000 left sitting in a 0–2% account while inflation ticks at 4% is losing real value. Multiply that by 12 months — and your “safe” money may have quietly lost $40 or more without you noticing.

Why “Safety” Can Be a Dangerous Illusion

Psychologically, cash feels good. It’s tangible. It’s there. It’s not red or down 20% like a bad stock pick.

But this emotional comfort hides a brutal reality:

“If inflation is 4% and your savings account pays 1%, you’re losing 3% a year just by doing nothing.”

Over a decade, that 3% loss compounds into over 25% of your purchasing power gone.

So yes — cash protects you from market volatility. But it exposes you to guaranteed value erosion.

The Real Role of Cash: Strategic Liquidity

In 2025, smart investors don’t see cash as a long-term asset. They see it as a strategic tool:

- 💼 For timing opportunities

- 🧯 For absorbing shocks

- 💡 For staying calm while others panic

It’s liquidity, not a growth vehicle. It buys time, not wealth.

The trick is not to abandon cash, but to limit its role. Your cash shouldn’t work harder than your investments — but it shouldn’t be asleep either.

Cash in a Crisis: What We Learned from 2020–2024

During global crises (COVID-19, Ukraine war, U.S. banking tremors), those who had access to cash survived. They paid bills. They bought assets at cheap prices. They avoided fire sales.

So while inflation is dangerous, illiquidity is worse.

Lesson? Have cash — but cap it. And make it work in parallel:

- Pair your emergency fund with gold or T-bills

- Use crypto or diversified ETFs for inflation protection

- Don’t let emotional fear dictate a 100% cash strategy

Final Verdict: Is Cash Still King in 2025 or 2026?

No. Not anymore.

In 2025 or 2026, cash is not king — but it’s still a valuable advisor.

It won’t protect you from inflation.

It won’t grow your wealth.

But it will give you the flexibility to act, adapt, and avoid ruin.

The key is balance. Not all cash is bad — but too much cash is silently dangerous. If you want your money to grow and your future to be safe, cash must become a small part of a bigger strategy — not the entire plan.

Cash vs. Inflation: The Invisible Tax on Your Wealth

Every time you hold cash in your wallet, bank account, or money market fund, you’re effectively making a bet against inflation. Unfortunately, in 2025, that bet hasn’t been paying off.

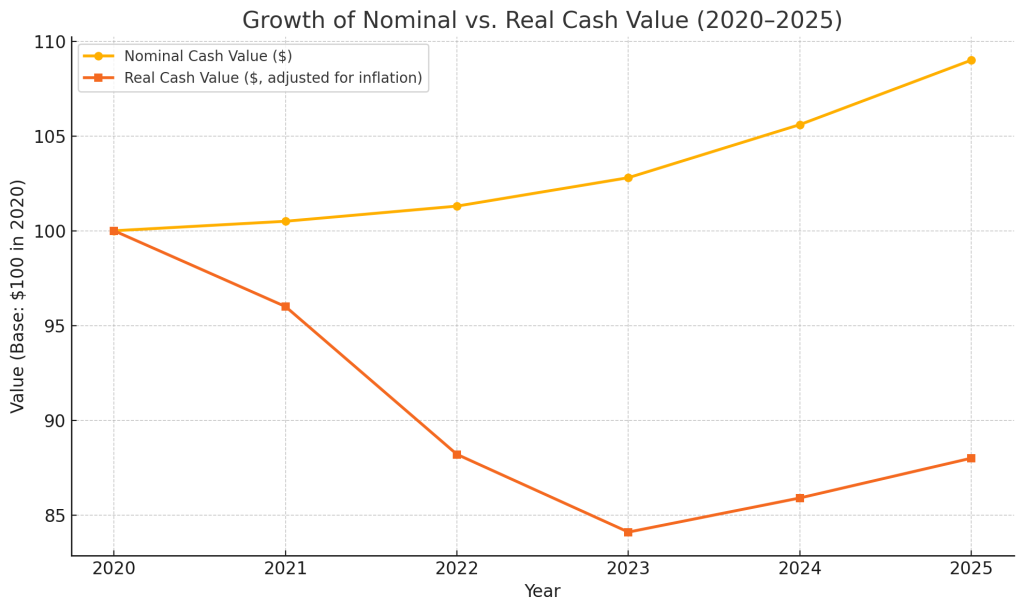

Inflation doesn’t need to be hyperinflation to do damage. Even modest inflation, say 3% annually, cuts your purchasing power in half over 24 years. At 4–5%, that timeline drops drastically. This means that holding large amounts of idle cash is guaranteed loss in real terms.

Let’s put that into numbers:

- $10,000 in cash with 0% interest and 4% inflation =

➤ $6,700 real value after 10 years

Compare that to investing in a conservative asset like Treasury Inflation-Protected Securities (TIPS), or even a simple dividend ETF, and the difference becomes staggering.

So, is cash risk-free? Technically yes, from a volatility standpoint. But it’s not reward-free, and it’s definitely not erosion-free.

Why So Many Still Hold Too Much Cash in 2025

Despite decades of financial education, millions continue to hoard cash in:

- Low-interest savings accounts

- Physical currency “under the mattress”

- Idle checking balances

Why? Because cash feels safe. There’s no red line going down like in Bitcoin or stocks. It gives control and clarity. That psychological benefit can’t be ignored — but it comes at a steep price.

Even in 2025, with AI-powered robo-advisors, crypto wallets, and instant ETF apps, many households and small businesses still have over 50% of their liquid assets sitting as cash.

This is one of the great silent crises in personal finance today.

The Role of Cash in a Diversified Portfolio

Let’s be clear: You do need cash. Just not too much.

In 2025 – 2026, cash is best used for:

🔸 Short-term liquidity: Pay bills, cover emergencies

🔸 Market opportunity funds: Wait for good entry points in crypto, stocks, or gold

🔸 Risk dampener: When paired with volatile assets, cash can smooth out the ride

Think of cash as your financial brakes. You don’t want to drive without them. But you also don’t want to ride the brakes down the entire mountain and wonder why you never sped up.

A better model?

60% long-term assets, 20% moderate-risk, 10–20% cash or near-cash depending on your goals.

Alternatives to Holding Pure Cash

In 2025, investors and savers have more tools than ever. If you’re worried about inflation, here are better “cash-alike” options:

💸 High-Yield Savings Accounts

→ Still accessible, now with 4–5% APY from top fintech firms

→ Protects against mild inflation while maintaining liquidity

🏦 Treasury Bills & TIPS

→ Government-backed and inflation-adjusted

→ Short maturity options ideal for cash parkers

🪙 Stablecoins (e.g., USDC, DAI)

→ For crypto-savvy users

→ Can yield 3–8% via DeFi (Decentralized Finance) platforms

→ Requires careful risk management

🟨 Gold & Bitcoin

→ Not cash, but historically solid long-term stores of value

→ Useful for hedging against fiat currency debasement

These aren’t perfect substitutes. But they’re far better than letting cash sit idle for years.

Is Cash a Weapon or a Wound in 2025?

Cash, like any financial instrument, is neutral — it’s how you use it that defines its value.

In hands of a patient investor:

✅ It’s a weapon — ready to strike when the market offers a discount.

In hands of a fearful saver:

🚫 It’s a wound — slowly bleeding wealth while giving the illusion of safety.

That’s why in finance, strategy beats instinct.

What Central Banks Are Teaching Us About Cash

It’s not just individuals. Central banks around the world are adjusting their own cash strategies. Why?

- High inflation → Tight monetary policy

- High interest rates → Safer yield on cash

- But also: risk of overexposure to fiat currencies in uncertain global macro climate

Many nations are increasing gold reserves, diversifying away from USD reserves, and some (like El Salvador) continue holding Bitcoin. This global behavior shift shows that even the largest institutions no longer treat cash as an untouchable safe haven.

Final Thoughts: Cash in 2025 — A Necessary Evil or Strategic Ally?

So, what’s the conclusion?

🟨 Cash is no longer king.

🟨 But cash is not dead either.

🟨 It’s a situational asset — valuable in moderation, dangerous in excess.

If you’re saving for a rainy day, cash is your umbrella.

If you’re building wealth, too much cash is a ball and chain.

Hold it with purpose, not out of fear. Read our article on how to allocate your cash holdings.

In 2025, cash is no longer the undisputed king of finance. But it’s not dead either. Its role has shifted — from being the dominant store of value to becoming a strategic tool in the hands of thoughtful investors. Whether it protects or damages your financial well-being now depends entirely on how you use it.

For those saving toward a short-term goal or simply trying to sleep well at night, cash offers clarity and stability. It’s the financial equivalent of a good umbrella — reliable when the skies darken. But for those aiming to build long-term wealth or outpace inflation, too much cash can become a drag — more of a ball and chain than a cushion.

What’s critical to understand in 2025 and 2026 is that cash must be held with intention. Not out of fear, and not just because it feels safe. When used as part of a wider, dynamic strategy — to time market opportunities, to hedge against volatility, or to support short-term liquidity — cash proves its value. But when it becomes a default, passive holding, it quietly erodes wealth and delays progress.

Even the world’s largest institutions are rethinking their cash exposure. Many central banks have begun diversifying away from traditional reserves like the US dollar and are increasing their gold holdings or experimenting with Bitcoin. This global shift reflects growing awareness that over-reliance on fiat cash, especially in times of high inflation or economic uncertainty, is no longer wise.

So ultimately, cash in 2025 and 2026 is best understood as a situational asset. It can be a powerful ally or a silent saboteur. What determines which it becomes is not the market — but your mindset and strategy. Holding cash isn’t a sin. But holding too much, for too long, without a plan? That’s where the real danger lies. Here is a case scenario why US dollar will not collapse too much further.

Related posts:

How to Invest During an Election Year: Stocks, Gold, Crypto, or Cash? (2026)

How to Invest During an Election Year: Stocks, Gold, Crypto, or Cash? (2026)

Where to Park Your Cash in 2025–2026: Not All Savings Are Equal

Where to Park Your Cash in 2025–2026: Not All Savings Are Equal

High-Yield Alternatives to Cash in 2025–2026: Where Smart Investors Park Their Money

High-Yield Alternatives to Cash in 2025–2026: Where Smart Investors Park Their Money

Cash Reserves: How Much Should a Small Business Keep on Hand in 2026–2027?

Cash Reserves: How Much Should a Small Business Keep on Hand in 2026–2027?

1 thought on “Is Cash Still King in 2025-2026?”

Comments are closed.