In an era defined by economic uncertainty, inflation concerns, and geopolitical instability, investors are flocking to tried-and-true hard assets. Two of the most popular? Gold and real estate.

But as we enter 2026 and look ahead to 2027, a critical question looms:

Which of these assets is the better long-term hedge against inflation, market volatility, and global risk?

Let’s compare the pros, cons, and outlooks of both — and help you decide which strategy may be smarter for protecting wealth in the years ahead.

Why Investors Are Focusing on Hard Assets Again

After a decade of growth in tech stocks, crypto, and low-interest cash accounts, 2025 marked a clear shift back toward tangible, real-world assets. That’s because:

- Inflation remains elevated, even as central banks fight to contain it

- Interest rates are still relatively high, making borrowing for real estate trickier

- Global instability (wars, elections, supply chain risk) is pushing investors toward safe-haven plays

- Fears of de-dollarization and fiat instability are growing

In short, both gold and real estate are back in the spotlight. But they play very different roles — and come with different risks and benefits.

Gold in 2026–2027: The Safe-Haven Metal Still Holds Power

Pros:

- Global liquidity — easy to buy/sell anywhere

- Hedge against currency devaluation

- Outperforms in crises (wars, banking collapses, etc.)

- No counterparty risk — you own it outright

- Now easier to access via ETFs, online dealers, and vault storage

Cons:

- No yield or rental income

- Short-term volatility can scare off new investors

- Value largely psychological — driven by fear, demand, and global uncertainty

2026–2027 Outlook:

- Gold reached record highs above $3,400 in 2025

- Most analysts believe it still has room to run in coming years

- Could benefit from U.S. election volatility, continued inflation, and central bank buying

- Especially popular among retirees and global investors seeking wealth preservation

Real Estate in 2026–2027: Inflation-Resistant but Complex

Pros:

- Generates rental income or cash flow

- Tax advantages (depreciation, deductions, 1031 exchanges)

- Tangible asset with long-term value

- Often keeps pace with inflation — rents rise with prices

- Can be leveraged for appreciation and equity growth

Cons:

- Illiquid and hard to sell quickly

- High interest rates may hurt affordability and pricing

- Local market risk (oversupply, taxes, tenant risk)

- Requires active management or property partners

- Less accessible for average investors — especially for international properties

2026–2027 Outlook:

- Mixed. Some markets may soften due to higher borrowing costs

- Still strong demand for multifamily housing, REITs, and vacation rentals

- May underperform if economy enters recession or rate environment stays high

Performance Comparison: Historical Returns and Volatility

Let’s look at some basic performance metrics:

| Asset | Avg Annual Return | Volatility | Liquidity | Income Potential |

| Gold | 7–10% (long-term) | Moderate | High | ❌ None |

| Real Estate | 8–12% (U.S. avg) | Low–Moderate | Low | ✅ Yes |

Gold wins on liquidity and crisis protection.

Real estate wins on income and tax efficiency.

But it’s not just about performance. It’s about what kind of protection you’re seeking.

What Type of Investor Should Favor Gold?

- Near or at retirement age

- Concerned about currency risk or U.S. dollar weakness

- Looking to hedge stock market volatility

- Interested in international or mobile wealth

- Prefers passive, low-maintenance assets

Who Should Favor Real Estate?

- Younger or middle-aged investors with time to manage properties

- Seeking income from rents or cash flow

- Willing to take on leverage/mortgages

- Focused on local markets or REIT investing

- Looking for long-term wealth-building with tax shelter

Can You Hold Both? Absolutely.

Many financial advisors suggest that gold and real estate work best together. They complement each other:

- Gold hedges against financial collapse and currency issues

- Real estate grows wealth and pays income over time

Example Portfolio:

- 50% stocks (diversified)

- 25% real estate (REITs, rental, crowdfunding)

- 15% gold (ETF or physical)

- 10% cash/crypto/alternatives

In a world of increasing complexity, having multiple hedges is often better than relying on one.

Emerging Trends to Watch

- Tokenized real estate — fractional ownership via blockchain

- Gold-backed stablecoins — more digital access to gold

- Real estate REITs vs. direct ownership — passive vs. active

- Central bank gold accumulation — signaling long-term bullishness

- Global migration — real estate demand shifting internationally

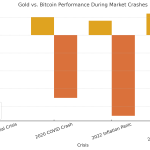

Historical Crisis Performance: How Did They Hold Up?

Investors often look to past crises to gauge how assets might behave during future uncertainty. Here’s how gold and real estate performed during some major shocks:

| Crisis | Gold Performance | Real Estate Performance |

| 2008 Financial Crisis | ✅ Rose 5–10% | ❌ Fell 20–30% in many markets |

| COVID-19 Crash (2020) | ✅ Spiked to record highs | ⚠️ Initially fell, then rebounded in 2021 |

| Stagflation 1970s | ✅ Tripled in value | ✅ Held up but not as strong as gold |

| 2022–2025 Inflation Cycle | ✅ Hit new highs above $3,400 | ⚠️ Mixed: hot markets boomed, others slowed down |

Conclusion:

Gold tends to outperform during high fear or recession environments.

Real estate is more sensitive to interest rates and credit access.

Global vs. U.S. Perspectives

In the United States, both gold and real estate remain popular wealth vehicles — but their dynamics are very different abroad.

Gold:

- In countries like India, Turkey, and China, gold is deeply embedded in culture and savings.

- Central banks across emerging markets are buying gold in record amounts to reduce reliance on the U.S. dollar.

🏘 Real Estate:

- In Europe and Asia, real estate often comes with heavy taxes or restrictions on foreign ownership.

- U.S. property remains a magnet for global investors, but high rates and local laws are starting to limit inflows.

Key Point:

Gold is a universal store of value, while real estate depends heavily on local politics, economies, and laws.

Millennials & Gen Z: Which Do They Prefer?

As younger generations enter their peak earning years, they’re reshaping the landscape of long-term investing.

🟨 Gold:

- Surprisingly gaining traction among Gen Z via digital gold, ETFs, and crypto-backed metals

- Viewed as an anti-establishment hedge by some

🏠 Real Estate:

- Still highly desired, but many younger buyers are priced out of major markets

- Fractional real estate apps, REITs, and co-living models are emerging as alternatives

Result:

Younger investors want exposure to both, but often start with digital or fractional versions before committing large capital.

Unique Risks to Consider

Each asset class comes with its own risks that are often overlooked:

⚠️ Gold Risks:

- Prices driven by emotion, not cash flow

- Manipulation or over-leveraged ETFs may distort real value

- Storage and insurance costs if held physically

⚠️ Real Estate Risks:

- Vulnerable to natural disasters, local policies, rent controls

- Tenant risk (non-payment, vacancies)

- Illiquidity during market downturns or emergencies

Being aware of these risks helps determine which asset fits your personal risk tolerance and timeline.

Where Are the Best Opportunities in 2026–2027?

Gold:

- Central bank demand continues to rise

- Potential for price breakouts above $3,500 if geopolitical tensions escalate

- Easier than ever to own across borders, especially with tokenized gold or ETFs

Real Estate:

- Secondary U.S. cities (e.g., Tampa, Boise, Raleigh) may outperform overpriced metros

- Vacation rentals and international properties (Mexico, Portugal, Thailand) are seeing demand from digital nomads and retirees

- Farmland and land banks gaining traction as alternative inflation hedges

Tax Advantages and Legal Framework: Which Asset Wins?

When comparing long-term hedges, it’s not just about price appreciation — the tax efficiency and legal flexibility of each asset class matter just as much.

Gold:

- In many countries, capital gains taxes apply on profits when gold is sold.

- However, ETFs and gold IRAs (in the U.S.) can offer tax-deferred growth, especially for retirement-focused investors.

- Gold is also a private, portable asset. In some jurisdictions, it can be passed on with fewer inheritance complications than real estate.

Real Estate:

- Real estate often offers stronger tax breaks — especially in the U.S.:

- Mortgage interest deductions

- Depreciation write-offs

- 1031 exchanges (to defer taxes by swapping properties)

- Landlords can also deduct maintenance, repairs, and property taxes.

- But real estate is also heavily regulated and subject to local zoning, tenant laws, and estate taxes that can complicate ownership or transfer.

Verdict:

For active investors or income seekers, real estate may provide stronger tax sheltering — but it comes with more paperwork and jurisdictional complexity.

Gold is simpler, more liquid, and easier to hold discreetly, but less tax-efficient unless used within structured accounts.

Liquidity and Exit Strategy: Selling When You Need To

The ability to sell quickly and efficiently is often overlooked — until it matters.

Gold:

- Extremely liquid in all forms:

- Physical coins/bars can be sold to dealers instantly.

- *ETFs and digital gold can be liquidated in seconds.

- No buyer negotiations, no agents, no inspections.

Real Estate:

- Highly illiquid, especially in down markets.

- Selling property involves:

- Listing it

- Finding a buyer

- Inspections

- Possible financing delays

- Closing costs, agent fees, legal docs

- In a crisis, your property may lose value or take months to sell.

Key Insight:

Liquidity is one of gold’s greatest advantages.

If you value flexibility, portability, or quick exit options, gold is the winner.

If you’re seeking long-term yield and leverage, real estate wins — but you must be prepared for slower exits.

Barriers to Entry: How Easy Is It to Start with Gold vs. Real Estate?

Gold: Lower Entry Barriers

- You can start investing in gold with as little as $50–$100, whether buying physical coins, fractional bars, or digital tokens.

- There are no credit checks, no legal documents, and no brokers needed.

- You don’t need to manage it — gold doesn’t need repairs, tenants, or insurance.

- Great option for new investors, retirees, or people living abroad.

Real Estate: High Capital & Knowledge Requirements

- Even a basic rental property in 2026–2027 requires:

- Significant upfront capital (down payment + closing costs)

- Credit approval

- Legal/title fees

- Ongoing property taxes, maintenance, and possible tenant issues

- Knowledge of the local market is essential — and mistakes can be costly.

- In some countries, foreign buyers face restrictions, adding to complexity.

Bottom Line:

Gold has very low friction for new investors.

Real estate can offer much higher returns — but only if you have the capital, time, and expertise to manage it effectively.

Final: Which Is the Better Hedge in 2026–2027?

There is no universal winner — only the better fit for your goals, timeline, and risk profile.

- If you value liquidity, stability, and long-term crisis hedging, gold shines brighter.

- If you seek income, appreciation, and tax advantages, real estate delivers more.

But in a world that’s shifting rapidly, the smartest play may be this:

Real Diversification Means Holding Both

If you’re investing for long-term security — especially for retirement — it’s worth remembering this:

Real estate builds wealth through time and leverage. Gold is also a waiting game. Hold both, in the right proportions.

How to Combine Both Assets in a Balanced Portfolio

For many investors, the best approach isn’t choosing between gold and real estate — it’s owning both. Gold offers liquidity, global portability, and rapid response to macro crises, while real estate delivers cash flow, inflation protection, and physical utility. A diversified strategy might allocate 5%–15% of portfolio value to gold (or gold ETFs), while also holding one or two income-generating properties or REITs. This allows investors to hedge against both monetary and economic shocks. As we head into 2026–2027, blending the stability of real estate with the defensive qualities of gold could be the most prudent path to long-term wealth preservation.