The U.S. debt crisis is no longer a distant warning on the horizon — it’s now a central force reshaping global markets, monetary policy, and investor behavior. As of late 2025, the national debt has surpassed $37 trillion, with interest payments alone expected to exceed $1.3 trillion annually by mid-2026.

This staggering trajectory has prompted a shift in how investors think about safety, inflation protection, and long-term store of value. As debt fears accelerate, two alternative assets — gold and Bitcoin — are once again at the center of debate. But which one is likely to outperform if the debt spiral continues? And how should you position your portfolio for what could be a major macro reset in 2026–2027?

Let’s explore the implications.

The U.S. Debt Picture in 2026: Too Big to Ignore

In 2026, the debt problem is not just about size — it’s about unsustainability.

- Total U.S. debt: Over $37 trillion and rising.

- Debt-to-GDP ratio: Now above 127%, approaching the post-WWII record.

- Interest payments: Could soon exceed all defense spending.

- Global buyers: Foreign central banks are quietly reducing exposure to U.S. Treasuries.

This situation places enormous pressure on the Federal Reserve and the U.S. Treasury. The Fed must choose between keeping interest rates high to fight inflation — which increases the cost of borrowing — or cutting rates to ease the debt burden, risking another wave of inflation.

This dynamic creates a credibility trap, where the U.S. risks both default via inaction or devaluation via money printing. Either scenario shakes confidence in fiat currency systems and opens the door for gold and crypto alternatives.

Gold: The Traditional Hedge in a Fiscal Storm

Gold has always played the role of the calm elder in times of fiscal chaos.

✅ Why Gold Still Works:

- No counterparty risk: Unlike bonds or currencies.

- Trusted globally: Central banks still stockpile it.

- Proven history: Gold surged after every major debt expansion (e.g., post-2008, post-COVID).

📈 Central Banks Are Buying:

According to the World Gold Council, central banks bought over 1,000 tons of gold in 2023 and 2024 — the highest on record — with China, India, and Russia leading the charge.

This trend reflects the growing distrust of the U.S. dollar’s long-term value and the desire for real assets in an age of excessive money creation.

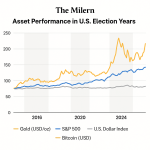

📊 Gold Performance During Debt Surges:

| Crisis Period | U.S. Debt Increase | Gold Price Change |

| 2008–2011 (GFC) | +$5.5T | +92% |

| 2020–2022 (COVID) | +$6.7T | +33% |

| 2023–2025 (post-COVID) | +$4.8T | +18% |

While gold may lack explosive returns, it provides stability, especially when traditional assets fall.

Bitcoin: The Digital Hedge Against Debt and Debasement

Bitcoin was born out of the 2008 financial crisis, specifically as a response to central banks printing trillions to rescue the system. Its appeal is rooted in finite supply (21 million coins) and independence from governments.

🧠 Why Bitcoin Is Gaining Traction:

- Scarcity narrative: “Digital gold” with hard-coded limits.

- Decentralized: Not controlled by any state or institution.

- Mobility and censorship resistance: Can be stored, moved, and accessed without banking intermediaries.

As governments print more to finance deficits, Bitcoin acts as an insurance policy against fiat debasement.

📉 But It Comes With Volatility

Bitcoin is notoriously volatile — capable of dropping 50% in months during corrections. This scares many conservative investors. Yet, over a long horizon, it has outperformed nearly every other asset class.

| Year | U.S. Debt Change | BTC Price Change |

| 2020 | +$4.5T | +305% |

| 2022 | +$1.4T | –65% |

| 2023 | +$1.7T | +160% |

| 2024 | +$1.5T | +21% |

Volatility cuts both ways. The key is position sizing, not prediction.

Let’s continue with:

- Investor strategies and allocation ideas for 2026–2027

- Likely monetary policy pivots and how gold/BTC would react

- Which will perform better long-term: gold or Bitcoin?

- Final summary and conclusion

Gold vs. Bitcoin in 2026–2027: Which One Holds Up Better?

Both gold and Bitcoin have compelling narratives in a debt-driven world, but they serve different psychological roles in investor portfolios.

| Feature | Gold | Bitcoin |

| Age | Over 5,000 years | 15 years |

| Volatility | Low | High |

| Liquidity | Very High | High (growing) |

| Institutional Support | Strong (central banks) | Growing (ETFs, hedge funds) |

| Supply | Inflationary but finite | Strictly finite (21M coins) |

| Custody Options | Physical, ETFs, vaults | Wallets, exchanges, ETFs |

| Regulation Risk | Low | Medium (still evolving) |

| Black Swan Resilience | Very High | Moderate (tech, legal risk) |

If the U.S. debt crisis escalates — especially via inflationary money printing or geopolitical shocks — both assets could perform well, but for different reasons.

- Gold shines in fear-driven environments and in institutional flight to safety.

- Bitcoin tends to rally in periods of dollar weakness, tech optimism, and liquidity surges.

Investment Strategy: Allocating Between Gold and Bitcoin

Rather than choosing just one, savvy investors often allocate to both, balancing upside with stability.

🔁 Suggested Strategic Allocation (as of 2026):

| Risk Profile | Gold (%) | Bitcoin (%) |

| Conservative | 10% | 2% |

| Balanced | 7% | 7% |

| Aggressive | 4% | 15% |

Your allocation should reflect:

- Time horizon (short-term fear vs long-term growth)

- Liquidity needs (gold can be faster to liquidate during panic)

- Risk tolerance (can you stomach a 50% drop in BTC?)

Diversifying within the asset class is also smart:

- Bitcoin + Ethereum (for tech innovation)

- Gold + Silver (for industrial demand and affordability)

What Could Go Wrong? Major Risks to Watch

Both gold and Bitcoin offer protection from fiat instability — but they are not immune to broader market disruptions. Here are some major risks to keep in mind:

Gold Risks:

- Price suppression through derivatives or central bank sales.

- Rising real rates, which make non-yielding gold less attractive.

- Strong dollar rebound, which historically hurts gold prices.

Bitcoin Risks:

- Regulatory crackdown, especially in the U.S. or EU.

- Exchange vulnerabilities and wallet custody issues.

- Loss of narrative if inflation remains tame or tech fatigue sets in.

- Price manipulation via whale movements or ETF dynamics.

Being aware of these risks — and having an exit or rebalancing plan — is essential for any serious investor.

How to Prepare Your Portfolio for the Debt Crisis

If you believe the U.S. debt situation will deteriorate further in 2026–2027, doing nothing is not a strategy.

Instead, consider:

- Reducing exposure to long-dated U.S. bonds

- Adding hard assets like precious metals and real estate

- Allocating a percentage to Bitcoin or crypto ETFs

- Watching the Fed and Treasury for signs of policy shifts

- Keeping cash ready for high-volatility buying opportunities

The coming years could represent a generational turning point in how wealth is stored, protected, and transferred.

Let us explore real-world use cases, central bank behavior, and monetary system stress-testing.

Central Banks, CBDCs, and the Rise of “Hard” Money

One of the strongest signals that gold and Bitcoin may rise in prominence during a debt crisis is the behavior of central banks themselves.

In 2023 and 2024, central banks around the world bought more gold than at any time since 1950, with countries like China, India, Turkey, and Russia leading the charge. The trend is clear: many governments are diversifying away from the U.S. dollar and bolstering their reserves with physical assets that can’t be debased or frozen.

This is not speculation — it’s a quiet vote of no confidence in fiat systems.

And while gold has long been favored by central banks, a new contender is rising: Bitcoin.

While no central bank is yet holding BTC as a reserve asset (at least publicly), sovereign interest is growing. El Salvador made Bitcoin legal tender. Other nations, especially those locked out of SWIFT or facing U.S. sanctions, are exploring blockchain-based settlements, stablecoins, and even Bitcoin-backed bonds.

At the same time, we’re seeing the rollout of CBDCs (Central Bank Digital Currencies). Though marketed as “innovation,” many see them as a way to centralize control over money, increase surveillance, and limit private alternatives like Bitcoin and cash.

This creates a clear dividing line:

- Gold and Bitcoin = individual monetary sovereignty

- CBDCs = centralized monetary control

As global debt balloons and confidence in traditional systems erodes, expect more investors — especially Gen Z and Millennials — to migrate toward decentralized and hard assets.

Real-World Use Cases in a Crisis: How Gold and Bitcoin Have Reacted

Let’s zoom in on how both assets behave during real crises, not just theoretical ones.

🟨 Gold in Crisis:

- 2008 Financial Crisis: Gold surged from ~$700 to $1,900 in three years.

- 2020 COVID Panic: Brief dip, then new highs as QE exploded.

- Russia–Ukraine War (2022): Jumped as safe-haven demand soared.

- 2023–2024: Reached new highs near $2,400+ as inflation fears persisted.

Gold has shown a consistent pattern: in times of geopolitical and monetary panic, capital rotates into gold — especially from institutions and foreign governments.

₿ Bitcoin in Crisis:

- March 2020 COVID Crash: Dropped 50%, then surged 10x within 18 months.

- 2021–2022 Inflation Cycle: Reached $69,000 highs, then corrected sharply.

- Bank Collapses in 2023 (SVB, etc.): BTC rallied as faith in banks wobbled.

- Ongoing global de-dollarization: BTC increasingly viewed as an escape hatch.

Importantly, Bitcoin reacts faster and more violently, both up and down. Its price is driven by:

- Retail sentiment

- Liquidity trends

- Narrative momentum

- Network growth

Bitcoin is not yet the “gold of the internet.” But it’s getting closer, especially as its adoption base grows beyond just tech enthusiasts.

Behavioral Finance: Why Most Investors Fail to Use Either Asset Correctly

A major issue with both gold and Bitcoin is investor psychology.

Gold skeptics often ignore it until a crash happens — then they buy too late. They also expect gold to behave like a stock (it doesn’t), and sell too early when it moves sideways.

Bitcoin investors, on the other hand, often overestimate short-term gains and underestimate volatility. Many new investors panic-sell during drawdowns, only to re-enter near the top.

To use either asset effectively:

- You must have a long time horizon

- You must treat them as insurance, not speculation

- You must rebalance, especially after major price moves

- You must know why you hold them (inflation? currency collapse? diversification?)

This is not about being a gold bug or a crypto bro — it’s about prudence in an uncertain world.

Final Countdown: Gold or Bitcoin — or Both?

The U.S. debt crisis is not just a fiscal problem — it’s a monetary confidence problem. In that environment, gold and Bitcoin become more than investments. They become hedges against systemic failure.

Gold offers stability and legacy trust. Bitcoin offers growth and disruption.

You don’t have to choose. A wise portfolio in 2026–2027 may include both — with the right balance based on your goals, risk tolerance, and worldview.

As central banks print, politicians spend, and interest costs spiral, the best response isn’t fear. It’s preparation.