Global tensions are rising. With escalating conflicts in Eastern Europe, the Middle East, and Asia, many are asking a question once unthinkable: Could we be heading toward a global war?

Even without a formal World War III, the economic effects of sustained global conflict—disrupted supply chains, military spending spikes, energy shocks, and geopolitical fragmentation—are already rippling across markets.

So how do you protect your money?

In this article, we explore the smartest ways to prepare financially for global war or prolonged geopolitical crisis, weighing the pros and cons of gold, Bitcoin, cash, stocks, and bonds in a high-risk, high-uncertainty world.

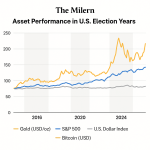

1. Gold: History’s Ultimate Crisis Hedge

When people lose trust in governments, currencies, and financial markets, they turn to gold. And for good reason:

- Thousands of years of value retention across wars, empires, and currency collapses

- No counterparty risk — it’s not tied to banks or governments

- Liquid globally, even in times of financial distress

In past conflicts, gold soared:

- During World War II, it protected purchasing power as paper currencies devalued

- In the 1970s (Cold War + inflation), gold rose more than 1,000%

Today, central banks are buying gold at record levels, and retail demand is surging in Asia and Europe. It remains the anchor of last resort.

Drawbacks?

- No yield or interest

- Can underperform during peacetime bull markets

2. Bitcoin: The Digital Escape Hatch

For a new generation of investors, Bitcoin is becoming “digital gold.” Its appeal during global instability is growing:

- Borderless and decentralized — no central authority can freeze it

- Scarce supply (only 21 million coins ever)

- Easy to store and transfer, even across borders in times of crisis

Bitcoin surged after the Ukraine war began in 2022, as Ukrainians and Russians both sought capital flight options. It’s increasingly being used in crisis zones and authoritarian regimes where traditional banking systems fail.

Pros:

- 24/7 access, even during banking blackouts

- Outperforms traditional assets in tech-savvy regions

Risks?

- Extreme volatility

- Not yet accepted everywhere

- Could be regulated or restricted during full-scale war

Still, many view it as a speculative hedge—a high-risk, high-reward layer of protection.

3. Cash: Liquidity and Optionality in a Crisis

Cash might seem boring, but in a crisis, cash is king—at least in the short term.

Why it matters in wartime:

- Gives you immediate flexibility to relocate, reallocate, or stock up on essentials

- Acts as a buffer against market crashes

- Useful in places where digital systems or banks may shut down temporarily

In global conflicts, ATMs can run dry, banks impose capital controls, and credit card systems freeze. Cash on hand (both local and foreign currency like USD or EUR) is crucial.

Drawbacks of holding too much cash:

- Loses value to inflation, especially during prolonged wars

- Generates no interest (or very little)

- Risk of theft or physical loss

Best approach: Hold enough physical cash for emergencies, plus short-term savings in high-yield accounts or money market funds that you can access quickly.

4. Stocks: Fragile but Strategic

Equities are a mixed bag during global war. In the early stages of major conflict or market panic, stocks usually drop sharply.

However, not all stocks behave the same:

✅ Defense contractors often rally

✅ Energy, food, infrastructure, and cybersecurity companies outperform

❌ Luxury, tech, travel, and banking stocks usually suffer

In WWII, the Dow Jones fell 30% early on — but by the end of the war, it had recovered and surged. In fact, wartime spending can drive industrial booms, especially for countries far from the front lines.

If you’re going to hold stocks during global conflict:

- Focus on value stocks, not speculative tech

- Consider dividend-paying companies with pricing power

- Favor sectors like energy, food, defense, and utilities

5. Bonds: A Changing Role in Wartime

Bonds used to be a haven in every crisis — but 2020s inflation changed that.

In global war scenarios:

- Governments often issue massive new debt to fund military budgets

- Central banks may suppress rates to finance this debt, hurting bondholders

- Inflation tends to rise, eroding bond returns

Long-term government bonds underperform in most high-inflation war periods. However, short-duration bonds or TIPS (inflation-protected bonds) can still play a role in conservative portfolios.

Key takeaways:

- Avoid long-dated sovereign bonds unless inflation is under control

- Stick to short-term high-quality debt or inflation-indexed bonds

Bar Chart – Performance of Gold, Stocks, Bonds, and Cash during major global crises like the Gulf War, 9/11/Iraq War, 2008 Financial Crisis, and Russia-Ukraine Conflict.

6. A Multi-Asset Strategy for Uncertain Times

If the threat of global war keeps rising, smart investors won’t go “all in” on any one asset.

Here’s an example crisis-resilient portfolio for 2025–2026:

| Asset Class | Allocation Range |

| Gold & Precious Metals | 15–25% |

| Bitcoin & Crypto | 5–10% |

| Cash & T-Bills | 10–20% |

| Stocks (Defensive + Energy) | 30–40% |

| Short-Term Bonds / TIPS | 10–20% |

This kind of allocation:

- Provides liquidity and downside protection

- Keeps upside potential through stocks and Bitcoin

- Is adjustable depending on your location and personal risk tolerance

7. Real Assets: Shelter from Monetary Turmoil

In prolonged global conflicts, especially if they escalate into currency devaluation or hyperinflation, real assets—like land, farmland, and even commodities—can offer powerful protection.

Why they matter:

- Tangible value: can’t be digitally seized or frozen

- Often appreciate during inflationary or wartime conditions

- Useful: farmland produces food; land holds utility and resale value

Examples of real assets that perform well in global crises:

- Farmland: food security becomes a national priority

- Energy infrastructure: pipelines, grids, utilities

- Industrial metals: copper, nickel, lithium — critical for weapons, batteries, and supply chains

Challenges:

- Illiquid: hard to sell quickly in a crisis

- Requires local stability and legal ownership protections

- Not accessible to small retail investors (though REITs and ETFs offer partial exposure)

Pie Chart – A suggested defensive asset allocation strategy (e.g., 25% gold, 20% cash, 15% crypto, etc.) for global conflict scenarios.

8. Geographic Diversification: Don’t Keep Everything in One Country

When global tension rises, where you hold your wealth matters almost as much as what you hold.

During past global wars, capital controls, seizures, and bank closures were common—even in democratic countries. Diversifying across jurisdictions helps reduce risk from:

- Domestic instability

- Currency collapse

- Government overreach or confiscation

Smart strategies include:

- International brokerage accounts (Switzerland, Singapore, UAE, etc.)

- Holding crypto with cold storage or multi-sig wallets

- Buying precious metals stored offshore

- Holding multiple currencies (USD, CHF, SGD)

This doesn’t mean fleeing your home country—it means preparing like a sovereign individual.

9. Psychology and Timing: War Often Comes in Phases

Investing in the shadow of war is not just about numbers. It’s about timing and psychology.

Many global conflicts do not erupt overnight. Instead, they build up in stages:

- Pre-War Tensions: Markets may ignore the signs.

- Sudden Shock: Invasion, collapse, or attack—markets drop sharply.

- Military Spending Ramps Up: Select industries rise.

- Prolonged Uncertainty: Inflation grows, markets swing.

- Resolution or Escalation: Winners and losers diverge.

The worst returns often come from panic selling during phase 2.

Staying emotionally grounded, diversified, and liquid helps investors avoid fatal mistakes—and even profit when others panic.

10. Defense Stocks and Military Contractors: Profit from the Unthinkable

One uncomfortable truth in wartime investing is this: defense stocks often soar while broader markets flounder.

From World War II to the Cold War to the Ukraine conflict, history shows that military buildup translates directly into profits for companies that supply the tools of war.

Key Sectors That Benefit:

- Aerospace & Defense: Think Raytheon, Lockheed Martin, Northrop Grumman, Rheinmetall.

- Cybersecurity: As cyberattacks escalate, companies like Palantir, CrowdStrike, and Darktrace gain relevance.

- Energy and logistics: Military campaigns run on oil, fuel, and efficient transport.

- Drones and robotics: The next frontier in military tech and surveillance.

Advantages:

- Strong government demand, often recession-proof

- Long-term contracts with guaranteed funding

- Pricing power during global insecurity

Risks:

- Ethical considerations (not all investors want to profit from war)

- Geopolitical black swan events—such as peace deals or budget cuts

Some investors opt for defense-themed ETFs like ITA (iShares US Aerospace & Defense) or DFND to gain diversified exposure.

11. Currencies in Conflict: Which Fiat Will Survive?

During global instability, currency volatility spikes, and local fiat currencies often take a major hit. Choosing the right currency exposure is crucial for preserving value.

Historically Strong Safe-Haven Currencies:

- U.S. Dollar (USD): Still dominant, despite inflation risks

- Swiss Franc (CHF): Low debt, strong institutions, neutrality

- Singapore Dollar (SGD): Respected in Asia-Pacific finance

- Norwegian Krone (NOK): Backed by energy exports and sovereign wealth

At-Risk Currencies:

- Euro (EUR): Vulnerable due to fragmented fiscal policy and geographic proximity to conflict zones

- Yen (JPY): No longer seen as a strong safe haven due to debt and demographic decline

- Emerging market currencies: Most are highly exposed to capital flight and trade shocks

Strategy:

- Keep some reserves in USD and CHF

- Consider multi-currency accounts or international brokerages

- Use Bitcoin or gold to reduce reliance on any single national currency

You’re not just investing in companies—you’re investing in the strength of the nation that prints your money. In global war, currency diversification is insurance.

Bar Chart – Currency Resilience Index showing which global currencies historically perform best as safe havens during crises (e.g., CHF, USD, SGD).

12. The Role of Geopolitical Hedging Funds and War-Ready ETFs

A growing class of investment products is designed specifically for crisis-era portfolio construction.

Examples:

- BlackRock iShares Global Infrastructure (IGF): invests in utilities and public works

- SPDR S&P Kensho Future Security ETF (FITE): focuses on cybersecurity and defense

- VanEck Gold Miners ETF (GDX): provides leveraged exposure to gold through miners

- Cambria Global Tail Risk ETF (TAIL): uses options to hedge against stock market crashes

Hedge Funds:

Some hedge funds position themselves explicitly for geopolitical volatility—holding short equity positions, volatility trades (VIX), or commodity spreads based on political developments.

Though not accessible to all investors, they offer a view into how institutional capital prepares for risk-on headlines.

13. Real Estate in Wartime: Shelter or Liability?

Real estate can be both a refuge and a risk in times of global conflict.

Residential Property

In stable regions, residential real estate may act as a safe-haven asset, especially if located in countries likely to stay neutral or insulated from war. Properties in Switzerland, Canada, Scandinavia, or even parts of South America may retain value—and offer a literal place of refuge.

Note – if in this conflict Arctic becomes a battlefield real estate in Canada or Scandinavia may not be most desirable asset, but it depends on location. For example, in Ukraine, after war broke our real estate market in eastern Ukraine was depressed, while real estate market in west of Ukraine was booming because people were moving their assets into real estate in the west to preserve their wealth and because they were moving their families to a relative temporary safety of the western Ukraine.

However, as war continues this safe heaven also may not hold as war activities increasingly move also to the west of Ukraine, which is also increasingly within reach of ballistic missiles or drones.

But war can lead to:

- Property seizures or damages

- Massive insurance disruption

- Flight of tenants and declining rental income

Agricultural and Rural Land

Farmland and rural retreats are increasingly seen as strategic assets:

- Self-sufficiency potential (food, water, solar)

- Limited government targeting

- Preserved value in a crisis scenario

However, liquidity is low, and maintenance is high—so it’s not for everyone.

14. Cash and Liquidity: Why Dry Powder Matters

In any global emergency, cash is king—until it’s not.

You need immediate liquidity to:

- Relocate if needed

- Cover emergency expenses

- Buy discounted assets when others panic

A good rule: hold 3–6 months of expenses in cash equivalents, but consider splitting that across institutions and currencies (USD, CHF, physical cash).

Also useful:

- Prepaid debit cards (untraceable and useful during system failures)

- Offshore accounts in politically neutral jurisdictions

- Physical assets: emergency gold coins, backup crypto wallets, or precious metals in personal safes

Don’t assume banks will always work or that ATM lines won’t form. In crisis, access beats APY.

How it was during WWII?

Here is a chart showing the average annual real returns of major asset classes during World War II (1939–1945):

- Gold preserved value with modest gains.

- U.S. Stocks delivered small negative real returns due to uncertainty.

- Bonds performed slightly better than cash.

- Cash held its nominal value but lost purchasing power due to inflation.

- Real Estate offered slight positive real returns in certain markets.

Final Thoughts: Resilience Is the New Alpha

Global war—whether it erupts fully or just threatens to—forces investors to ask hard questions.

No one knows the future. But prudent preparation today can mean survival tomorrow, and even upside.

The right mix of:

- Gold for defense

- Bitcoin for sovereignty

- Cash for flexibility

- Stocks for long-term upside

- Geographic diversification for redundancy

…can help you sleep at night—no matter what headlines come tomorrow.

In a world where missiles might fly, financial missiles (like inflation, currency collapse, and capital controls) will strike first. Those who prepare today won’t just survive. They may thrive.