With traditional pensions vanishing and market uncertainty rising, more people are asking: Should I include Bitcoin, Ethereum, or other cryptocurrencies in my retirement strategy?

As financial systems evolve, crypto has gone from a fringe speculation to a mainstream debate. But does that mean it’s safe—or smart—for retirement?

In this article, we’ll examine the real risks and potential rewards of using crypto in retirement portfolios in 2025 and beyond. You’ll see who it’s best suited for, what allocation levels make sense, and how to manage volatility.

Why Retirement Investors Are Looking at Crypto

- Inflation and Fiat Risk: After multiple years of inflation above central bank targets, many retirees are losing confidence in fiat currencies. Bitcoin and Ethereum are being considered as digital alternatives that can’t be printed away.

- Diversification Beyond Stocks and Bonds: Traditional 60/40 portfolios have suffered real losses in recent years. Crypto offers a new asset class with different drivers than stocks, bonds, or even gold.

- High Long-Term Upside: Bitcoin is still up over 1000% from 2017 levels. Ethereum powers much of the decentralized finance (DeFi) world. Even a small allocation can massively shift a portfolio’s long-term outcome.

- Institutional Acceptance: Fidelity, BlackRock, and Schwab now offer crypto ETFs and custodial services. Retirement platforms like iTrustCapital and Alto IRA let you allocate directly to BTC or ETH.

Risks You Must Understand

- Volatility: Bitcoin has fallen over 50% multiple times in the last decade. Large drawdowns are part of the crypto cycle and can be emotionally difficult for investors unused to extreme price swings.

- Impulsive Selling: Due to crypto’s fast-moving, 24/7 nature, many investors panic during downturns and lock in losses. Retirement investors must be disciplined and avoid emotional decisions.

- Regulatory Uncertainty: Especially in the U.S., crypto faces unclear tax rules and SEC scrutiny. Changes in policy can affect asset values quickly.

- Security: Self-custody demands technical knowledge. Hacks and scams are still frequent in DeFi. Mistakes in managing private keys can lead to permanent loss of funds.

- Correlation During Crashes: Crypto sometimes behaves more like tech stocks than like gold. It can fall sharply during global risk-off events.

- Knowledge Gap: Crypto is still a relatively new and evolving field. Investors must be willing to dedicate time to understanding its mechanics and risks.

Crypto is not a substitute for a pension or fixed income stream. It’s a high-risk, high-reward satellite asset that must be approached with care.

Illustrative Volatility Comparison: Crypto vs Traditional Assets

Smart Ways to Include Crypto in Your Retirement Strategy

- Small Allocations (1–5%) For most retirement accounts, crypto should not exceed 5% of the portfolio. Even 1% can add upside without derailing stability.

- Use Crypto-Friendly Retirement Platforms Platforms like iTrustCapital, BitIRA, and Alto IRA allow direct crypto investing within tax-advantaged IRAs.

- Favor Bitcoin and Ethereum These two have the highest adoption, institutional support, and staying power. Avoid smaller tokens unless you have a very high risk tolerance.

- Rebalance Periodically If Bitcoin soars, trim it back to maintain your risk level. If it crashes, don’t panic sell—treat it like any other asset class.

- Consider Crypto ETFs for Simplicity The new Bitcoin and Ethereum ETFs offer indirect exposure, are easier to manage, and fit traditional IRAs and 401(k)s.

Who Should Consider Crypto in Retirement?

Younger Investors (30s–50s):

- Time horizon is long enough to ride out volatility.

- Can afford small allocations for asymmetric upside.

Tech-Savvy Investors:

- Comfortable with private keys, cold wallets, and DeFi tools.

- More likely to benefit from active participation in the crypto ecosystem.

Diversification Seekers:

- Looking for uncorrelated assets.

- Already have traditional stocks, bonds, and real estate.

Cautious Note: If you’re retiring in the next 1–3 years and need predictable cash flow, crypto should be minimized or avoided entirely.

More Thoughts

Crypto is no longer an outsider asset—but that doesn’t make it risk-free. As part of a diversified retirement plan, Bitcoin and Ethereum can offer potential upside and inflation protection. But they must be handled with care, not hope.

Used wisely, crypto can play a small but powerful role in your financial future.

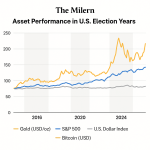

Historical Context: Crypto’s Evolution Into a Retirement Asset

Bitcoin began as a niche experiment in digital money after the 2008 financial crisis. Over the years, it has matured into a recognized asset with its own market cycles, trading infrastructure, and institutional access points. Ethereum introduced smart contracts and decentralized applications, expanding crypto’s use cases beyond “digital gold.”

By 2025, these assets have weathered multiple booms and busts—and they’ve survived. That resilience has prompted even traditional advisors to reconsider earlier skepticism.

In 2021, few retirement advisors would recommend crypto. By 2025, many recommend a cautious allocation.

The shift is subtle but significant.

How Crypto Compares to Other Alternative Retirement Assets

Let’s look at how crypto stacks up against other popular “non-traditional” retirement allocations:

| Asset | Pros | Cons |

| Gold | Inflation hedge, thousands of years of trust, low correlation | No yield, can underperform for years |

| Real Estate | Tangible, cash flow, appreciation potential | Illiquid, maintenance costs, bubbles |

| Commodities | Hedge against global instability, useful during inflation | Volatile, cyclical, hard to hold in tax-advantaged accounts |

| Crypto (BTC/ETH) | High upside, scarcity, digital-native, 24/7 markets | Extreme volatility, regulatory risks, security challenges |

The key takeaway: crypto belongs in the speculative growth bucket—not the income or capital preservation category. But that’s also what makes it valuable as a small addition to a larger retirement mix.

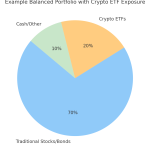

Portfolio Allocation Examples with Crypto

To visualize how crypto might fit into different retirement portfolios:

Conservative Investor (age 55+):

- 55% bonds

- 30% equities

- 10% real assets (real estate, gold)

- 5% crypto (BTC/ETH)

Moderate Investor (age 40–55):

- 50% equities

- 25% bonds

- 15% real estate/inflation hedges

- 10% crypto (BTC-heavy)

Aggressive Investor (under 40):

- 60% equities

- 15% bonds

- 10% alternatives

- 15% crypto (BTC/ETH and some altcoins)

These are examples, not recommendations—but they show that there’s no one-size-fits-all strategy. The key is understanding your risk profile and time horizon.

Crypto Allocation by Risk Profile (Suggested for Retirement)

Crypto Tax Considerations for Retirement Accounts

Crypto inside Roth IRAs or Traditional IRAs grows tax-deferred (or tax-free with Roths). This makes them ideal for:

- Active traders (no capital gains tax per trade)

- Long-term holders (tax-free growth potential)

But outside of retirement accounts, crypto is taxed like property in most jurisdictions:

- Capital gains tax on profits from selling

- No wash sale rule (as of 2025, in many regions), allowing tax-loss harvesting

- Reporting obligations with every transaction

To avoid headaches, most retirement investors prefer ETF-based crypto exposure or platforms that handle tax tracking automatically.

Why Crypto’s Volatility Is a Bigger Deal in Retirement

Even though price swings are expected in crypto, the stakes are different when you’re planning for retirement. Unlike younger investors who have time to recover from drawdowns, retirees don’t have the luxury of decades to wait for a rebound. When Bitcoin falls 60% in a matter of weeks, it can seriously damage your sense of security—even if you only had a small allocation.

The volatility alone isn’t the only issue—it’s the emotional toll. Many investors panic and sell during crashes, even when they know better. That’s especially true with crypto, where news cycles are intense and prices can move 10–20% in a single day. If you don’t have the stomach for extreme drawdowns, even a 3–5% exposure might feel like too much.

Retirement investors must ask: “Can I watch this part of my portfolio lose 50% without doing something rash?” If the answer is no, you may want to stick with ETFs or structured exposure instead of holding raw crypto assets.

Not All Crypto Is Created Equal

Another major risk is choosing the wrong coin. While Bitcoin and Ethereum dominate market cap and institutional interest, there are thousands of other cryptocurrencies—most of which are speculative or poorly maintained. Some vanish entirely within a few years.

Including crypto in your retirement doesn’t mean buying random tokens you saw trending on YouTube. It means doing your homework and sticking with the most proven assets. Even then, Ethereum is still undergoing upgrades, and Bitcoin is not without risks—it depends heavily on miner incentives, network security, and global regulation.

Before allocating even 1%, ask yourself:

- Is this asset widely adopted?

- Does it have strong developer and institutional support?

- Has it survived previous bear markets?

- How easy is it to custody safely?

For most retirement-minded investors, Bitcoin and Ethereum are the only two that should even be considered—and ideally through ETFs or regulated platforms.

Ways to Minimize Crypto Risk in Retirement

Managing crypto risk isn’t just about limiting the percentage in your portfolio—it’s about how you hold it and what you hold.

- Stick to Regulated Access Points:

ETFs, publicly listed trusts, and IRA-friendly platforms reduce the risk of technical errors or fraud. You don’t have to manage wallets, keys, or networks. - Set Hard Limits:

Decide ahead of time how much crypto your portfolio will hold. If Bitcoin doubles, rebalance to avoid overweighting. - Avoid Leverage and Complex Yield Products:

Some crypto platforms offer staking, yield farming, or synthetic asset exposure. These are high-risk strategies and usually inappropriate for retirement investors. - Treat Crypto Like Venture Capital, Not Cash

If it hits, great—but don’t count on it to fund your monthly expenses. - Diversify Within the Crypto Allocation (If Large Enough)

If your total crypto exposure exceeds 5–10% (which we don’t recommend for most), consider a mix of BTC, ETH, and possibly a stablecoin or infrastructure token—but only if you deeply understand what you’re doing.

Mindset Matters: Crypto and the Psychology of Retirement

Retirement isn’t just a financial transition—it’s a psychological one. You’re shifting from accumulation to preservation. That means your tolerance for risk, volatility, and uncertainty naturally shrinks.

This is where crypto can become a double-edged sword. The excitement of potential gains is real—but so is the anxiety of large drawdowns or unexpected news. Watching your crypto holdings swing 20–30% in a matter of days may not just hurt your portfolio—it can disrupt your peace of mind.

The key is not just to manage exposure, but to manage expectations. Crypto isn’t a safe haven like cash or bonds. It’s a speculative growth asset with a long time horizon. It requires emotional discipline, strategic thinking, and a willingness to learn.

If you view Bitcoin or Ethereum as a lottery ticket or a quick fix to boost returns, you’re setting yourself up for disappointment. But if you see crypto as a small piece of a larger, diversified retirement plan—one that includes income-producing assets and capital preservation tools—then it can serve a purpose.

Think of crypto not as a replacement, but as an enhancement. The goal is not to retire on crypto alone—but to use it, carefully and intentionally, as one possible lever in your long-term financial plan.