As global markets grow more volatile and inflation fears linger, more investors are turning to alternative safe-haven assets. Two stand out above the rest: gold and Bitcoin. One is the most time-tested store of value in history. The other is a digital asset born out of the 2008 financial crisis.

But what if you didn’t have to choose between them?

In this article, we’ll explore how to combine gold and Bitcoin in a modern portfolio — to hedge inflation, reduce systemic risk, and still benefit from asymmetric upside. Whether you’re building a retirement strategy or looking to preserve wealth, this dual-asset approach could be one of the smartest moves for 2026 and beyond.

Why Gold and Bitcoin Are Often Compared — But Serve Different Roles

Gold and Bitcoin are often framed as competitors. But that’s a false choice. In truth, they serve complementary purposes:

| Feature | Gold | Bitcoin |

| Age | Thousands of years | ~15 years (since 2009) |

| Form | Physical | Digital |

| Scarcity | Finite supply | Capped at 21 million |

| Inflation Hedge | Proven over centuries | Emerging use case |

| Price Volatility | Low–moderate | High |

| Adoption | Central banks, institutions | Retail, digital-native funds |

| Custody | Physical storage required | Self-custody or custodians |

Key takeaway: Gold is stability and legacy, Bitcoin is innovation and growth.

You don’t have to pick a side. Instead, the smart investor in 2026–2027 is learning how to blend them strategically.

Why Gold Alone May Not Be Enough Anymore

Gold has preserved wealth for centuries. But in today’s high-speed digital economy, it faces limitations:

- Limited price movement: While it protects purchasing power, gold often lags in performance.

- Storage and transport issues: Physical gold is expensive and inconvenient to move.

- Lack of yield: Gold doesn’t produce income or yield unless tokenized or leased.

Even central banks are exploring digital currency reserves — and that’s where Bitcoin enters the equation.

Why Bitcoin Alone Is Still Risky

Bitcoin offers potential for massive gains, but it comes with real risks:

- Extreme volatility: BTC can drop 20–30% in weeks.

- Regulatory uncertainty: Laws differ globally and change fast.

- Custody risk: Self-custody requires technical confidence; exchanges can be hacked.

- Correlated during crashes: BTC sometimes behaves more like tech stocks than gold.

Bitcoin isn’t yet a full replacement for gold — but it can supercharge your inflation hedge when used correctly.

What Happens When You Combine Gold and Bitcoin?

By combining both, you offset their weaknesses and amplify their strengths.

Benefits of a dual allocation:

✅ Hedge inflation with diverse tools (gold = slow burn, BTC = fast hedge)

✅ Reduce risk via uncorrelated cycles

✅ Prepare for both physical and digital economic shifts

✅ Add growth potential without betting the farm

Let’s say your portfolio is 10% “inflation hedge.” You could split that into:

- 5% gold

- 5% Bitcoin

This simple move diversifies your store-of-value hedge while avoiding overexposure to one asset.

Real-World Scenarios Where Gold + Bitcoin Shine

Here are some examples of how this duo works in real markets:

Scenario 1: Inflation Spikes

- Gold performs well as fiat weakens.

- Bitcoin may spike due to falling trust in central banks.

Result: Both assets rise, boosting your real returns.

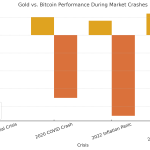

Scenario 2: Market Crash

- Bitcoin may crash with equities (as seen in 2020, 2022).

- Gold often holds or rises due to flight to safety.

Result: Gold stabilizes the portfolio while Bitcoin recovers later.

Scenario 3: Currency Crisis or Bank Freeze

- Gold protects offline purchasing power.

- Bitcoin enables cross-border transfers and capital flight.

Result: Each asset helps depending on the nature of the crisis.

How to Structure Your Allocation in 2026–2027

There’s no one-size-fits-all answer, but here are a few strategic setups:

- Conservative Investor

- 90% traditional portfolio

- 7% gold

- 3% Bitcoin

Purpose: Hedge inflation with minimal volatility

- Balanced Approach

- 80% traditional portfolio

- 10% gold

- 10% Bitcoin

Purpose: Hedge inflation and add growth potential

- Aggressive Growth with Hedge

- 70% traditional

- 5% gold

- 20–25% Bitcoin

Purpose: Bet on digital revolution with some stability via gold

Note: Rebalance every 6–12 months based on performance and market cycles.

Where to Buy and Store Each Asset

| Asset | How to Buy | Storage Options |

| Gold | Bullion dealers, ETFs (GLD, IAU) | Vaults, personal safes, gold IRAs |

| Bitcoin | Crypto exchanges, ETFs (IBIT, FBTC) | Self-custody (cold wallets), crypto IRAs |

For long-term portfolios, many investors now use gold IRAs and crypto IRAs like those from iTrustCapital or BitIRA.

Next: how to protect your combined holdings and navigate future risks.

How to Manage Risk With a Gold-Bitcoin Strategy

Even though gold and Bitcoin can complement each other well, risk management is still critical — especially in a volatile macro environment like 2026–2027.

- Avoid Overconcentration

Don’t bet too heavily on either gold or Bitcoin. While both are viewed as hedges, they can behave unpredictably. A blended approach works best when the allocation is reasonable and not overleveraged.

✅ Tip: Most investors keep total exposure to alternative assets (including gold, Bitcoin, silver, etc.) under 25% of their total portfolio.

- Rebalance Regularly

If Bitcoin doubles in a year and gold lags, your portfolio might become imbalanced. Periodic rebalancing helps lock in profits and keeps risk aligned with your goals.

⏳ Recommended: Rebalance every 6–12 months or when one asset moves more than 25% compared to the other.

- Keep Different Custody Plans

Don’t store both assets with the same institution or wallet. Gold is physical and often held in private vaults. Bitcoin should ideally be self-custodied using a hardware wallet, or stored through segregated accounts if using a custodian.

🔐 This ensures you’re protected from counterparty risk on both fronts.

- Diversify Across Asset Types

Gold and Bitcoin are part of the “store of value” sleeve, but they shouldn’t be your only hedges. Consider also:

- Treasury Inflation-Protected Securities (TIPS)

- Dividend-paying defensive stocks

- Real estate investment trusts (REITs)

- Commodities like oil, uranium, or agricultural ETFs

This layered strategy improves crisis resilience.

- Stay Educated on Regulatory Trends

Both gold and Bitcoin face evolving regulations globally. In 2026–2027, we could see:

- More central bank digital currencies (CBDCs)

- New rules on crypto taxation, capital controls, or KYC

- Shifting geopolitical sentiment around asset flight or financial surveillance

📌 Keep up with policy changes, especially if you live or invest across borders.

Strategies to Combine Bitcoin and Gold in a Portfolio

If you’re looking to hedge against inflation, currency devaluation, or geopolitical instability, combining Bitcoin and gold may offer a compelling balance of security and growth. However, integrating both assets effectively in a long-term portfolio requires a thoughtful approach.

- Allocation Strategies: How Much of Each?

- Conservative Approach

If you’re nearing retirement or are risk-averse, consider a 5–10% allocation total to both assets, split with a heavier emphasis on gold (e.g., 7% gold, 3% Bitcoin). Gold brings historical resilience, while Bitcoin adds a high-risk, high-reward component. - Balanced Growth Strategy

A 10–20% total allocation (e.g., 10% gold, 10% BTC or ETH) may suit those with a medium-term horizon who are seeking asymmetric growth but still value a traditional store of value. - Aggressive Growth

If you’re in your 30s or 40s with a long runway and a high risk tolerance, some investors allocate 20–30% or more to these alternative hedges—with Bitcoin often taking a larger share. This is speculative but could yield outsized returns over time.

In all scenarios, the key is not to overexpose your portfolio to either asset without regular rebalancing.

- When to Buy? Use Market Cycles to Your Advantage

Gold and Bitcoin often perform differently based on macro cycles:

- Buy Gold when interest rates are falling, inflation fears are rising, or geopolitical tensions increase.

- Buy Bitcoin during bear markets, accumulation phases, or post-halving periods when upside potential is historically strongest.

If you’re layering into both assets over time, using a dollar-cost averaging (DCA) strategy helps smooth out volatility and avoid emotional buying/selling.

- Storage and Security: Keep It Safe

While both assets can be self-custodied, they require different levels of technical setup:

- Gold: Physical bullion should be stored in a vault or insured depository. If held at home, a high-security safe and insurance are a must. Alternatively, consider allocated gold in trusted ETFs or digital gold tokens like PAXG.

- Bitcoin: Self-custody via hardware wallets like Ledger or Trezor is best for long-term holding. Avoid leaving large sums on exchanges. Learn how to back up seed phrases and consider multisig wallets for added security.

Pro Tip: Don’t rely on third parties unless you trust them deeply. If you do, choose regulated custodians with insurance.

- Rebalancing: Managing Volatility and Growth

Gold is historically more stable, while Bitcoin can gain or lose 30% in a week. If BTC surges and becomes 25% of your portfolio from an initial 10%, consider rebalancing to lock in gains. Similarly, if BTC drops significantly, consider adding to your position (if fundamentals are unchanged) to maintain your allocation target.

Rebalancing annually or semiannually helps you maintain discipline, reduce downside risk, and harvest profits from overperforming assets.

- Tax Considerations

- Gold is often taxed as a collectible in the U.S., with a long-term capital gains rate of up to 28%.

- Bitcoin is taxed as property, meaning short- and long-term capital gains rules apply depending on your holding period.

If held in tax-advantaged retirement accounts (like a Bitcoin IRA), gains may be deferred or even tax-free, depending on account type. Always consult a tax advisor.

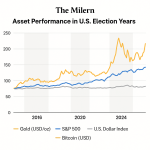

Historical Context: Why This Matters More in 2025–2026

We are entering an era where central banks are torn between cutting rates to stimulate growth and fighting stubborn inflation. At the same time, national debt levels are historically high, and the geopolitical order is shifting.

In such a climate, the 60/40 portfolio is being re-evaluated. Investors are increasingly looking for non-correlated assets that can preserve wealth under a wide range of scenarios. This is where gold and Bitcoin shine—each in its own way:

- Gold has protected wealth for over 5,000 years.

- Bitcoin is arguably the fastest-growing monetary network in history.

By combining the two, you gain exposure to both legacy and innovation, stability and growth, defense and offense.

Final Thoughts: A 21st Century Hedge Needs a 21st Century Mindset

Gold has served as the world’s universal store of value for millennia — but the digital age demands new tools. Bitcoin introduces programmable scarcity, mobility, and censorship resistance in a world moving toward digitized finance.

By blending gold’s historical strength with Bitcoin’s future-forward potential, you create a modern safe-haven strategy that covers both the old world and the new.

This isn’t about choosing sides. It’s about adapting wisely.

In 2026 and 2027, investors who diversify across eras — not just assets — will be best prepared to weather inflation, war, currency risk, and digital disruption.