With inflation rising and the cost of living surging across much of the West, many Americans and Europeans are asking a serious question:

Can I retire abroad with $500,000?

And if so — where would my money go the furthest?

The answer is yes — but only if you choose your destination wisely, account for local healthcare, and avoid common pitfalls. In this guide, we’ll explore the top countries to retire abroad with half a million dollars, the monthly income you can expect, and how far your nest egg can really stretch in 2025–2027.

Why More People Are Retiring Abroad in 2025

Several trends are driving a wave of interest in international retirement:

- High living costs in the U.S., Canada, and Western Europe

- Political and economic instability at home

- Desire for a better climate, healthcare, or slower pace of life

- The rise of remote banking, telehealth, and residency options

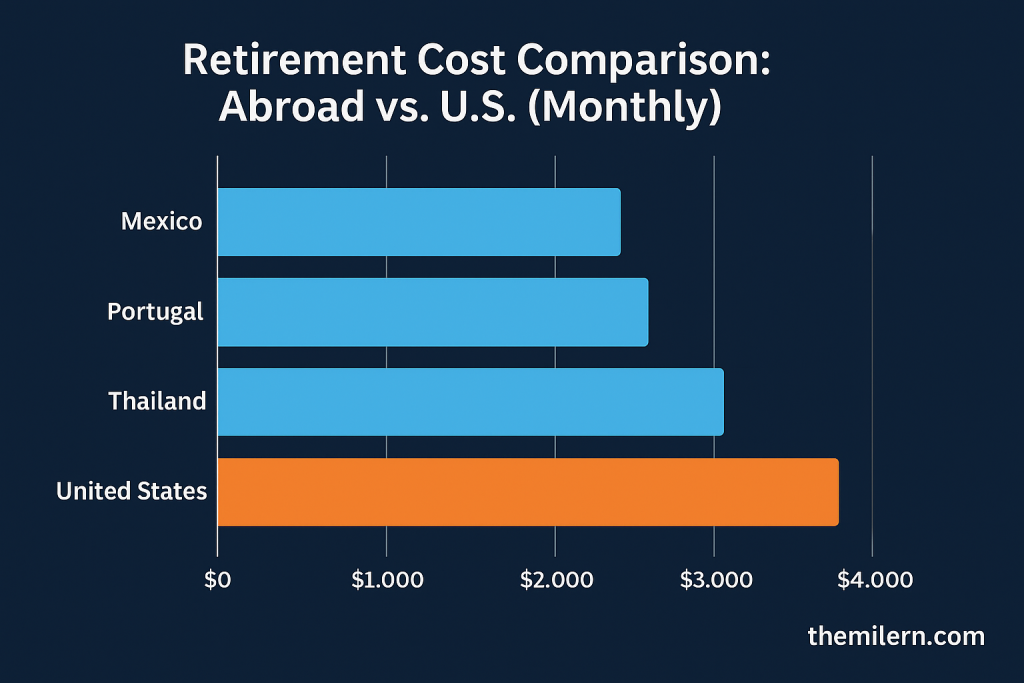

A $500,000 portfolio may no longer guarantee a long retirement in Los Angeles or London — but in Portugal, Mexico, or Thailand? You could live comfortably for decades.

What $500,000 Really Buys You in Retirement

Before naming countries, let’s break down what a $500,000 nest egg can support abroad:

| Retirement Duration | Annual Spending | Monthly Budget |

| 20 Years | $25,000/year | $2,083/month |

| 25 Years | $20,000/year | $1,666/month |

| 30 Years | $16,600/year | $1,383/month |

⚠️ Note: These figures assume no investment growth and a gradual drawdown of principal. With modest growth (e.g. 3–5%), your timeline can stretch longer — especially if paired with part-time income or Social Security.

Now let’s see where $1,300–$2,000/month can take you.

Top Countries to Retire Abroad with $500,000 (2025–2027)

🇵🇹 Portugal – A Top EU Destination

- Monthly Cost of Living: $1,200–$1,900 (for a couple outside Lisbon)

- Healthcare: Excellent public and private care

- Residency: D7 visa or retirement residency options

- Pros: EU access, safety, English widely spoken, mild climate

Portugal has become one of the best-balanced options for expats: affordable, culturally rich, and stable.

🇲🇽 Mexico – Close, Cheap, and Comfortable

- Monthly Cost of Living: $1,000–$1,600

- Healthcare: Affordable private care with U.S.-trained doctors

- Residency: Temporary resident visa available for retirees

- Pros: Proximity to the U.S., vibrant culture, diverse climates

Mexico is ideal for retirees who want to stay close to home but slash costs by 50–70%.

🇹🇭 Thailand – Tropical Living on a Budget

- Monthly Cost of Living: $800–$1,300

- Healthcare: Excellent private hospitals in Bangkok and Chiang Mai

- Residency: Retirement visa available (50+ years old)

- Pros: Low costs, world-class cuisine, warm weather

For retirees open to Asia, Thailand offers luxury-level living at budget prices.

🇬🇪 Georgia – Europe’s Underrated Gem

- Monthly Cost of Living: $700–$1,000

- Healthcare: Improving, private care recommended

- Residency: Easy visa-free stays or special permits

- Pros: Low taxes, fast-growing digital economy, safe

Georgia (the country) is an emerging hotspot for adventurous retirees and digital nomads alike.

🇨🇷 Costa Rica – Green, Peaceful, Stable

- Monthly Cost of Living: $1,400–$2,000

- Healthcare: High-quality private care

- Residency: Pensionado program (fixed income required)

- Pros: No military, eco-lifestyle, stable democracy

Costa Rica isn’t the cheapest — but offers unmatched tranquility and biodiversity.

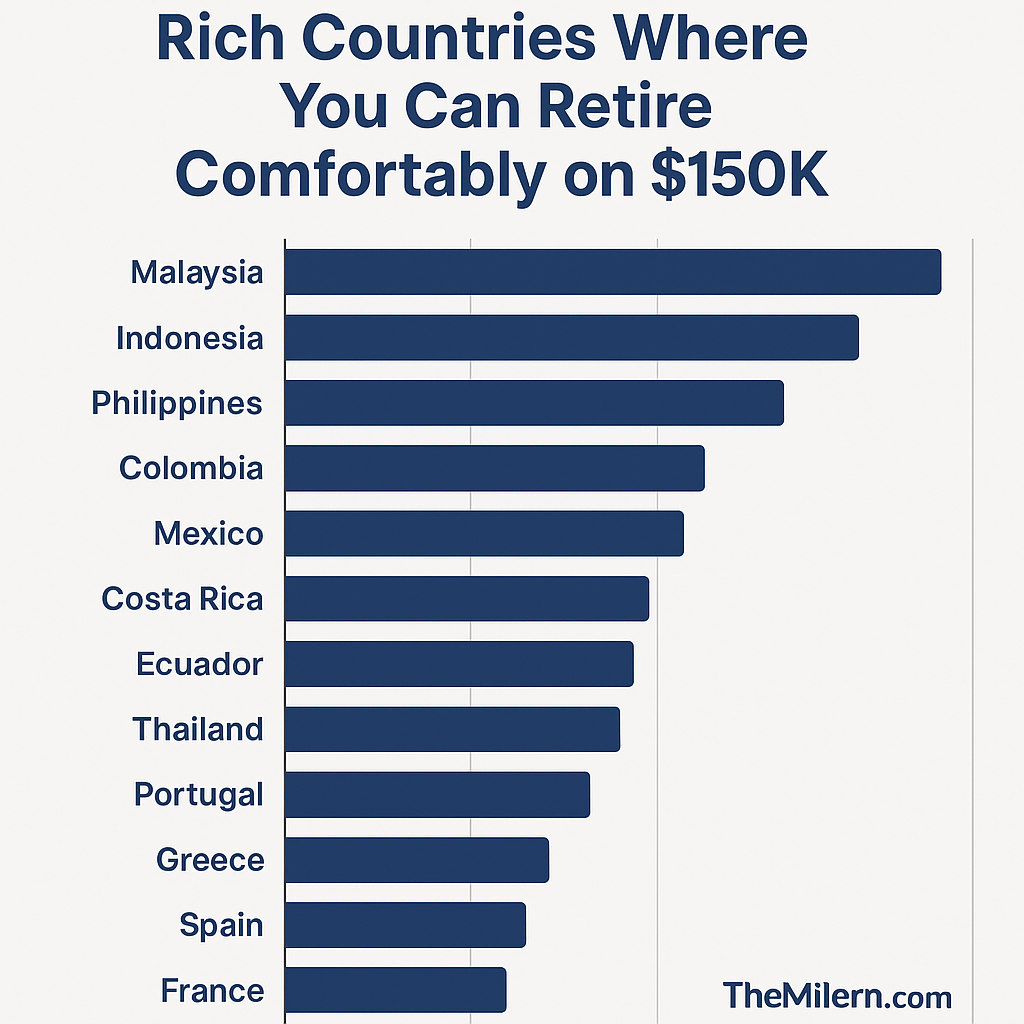

Here is a chart of annual costs of living in major countries.

“Rich Countries Where You Can Retire Comfortably with $500,000”

featuring realistic annual cost of living estimates across a variety of popular retirement destinations.

Taxes, Banking, and Residency: What You Need to Know

When retiring abroad, moving costs are just the beginning. You’ll need to plan for:

🧾 Tax Implications

- U.S. Citizens: Still must file with the IRS annually, even abroad. The Foreign Earned Income Exclusion (FEIE) won’t help retirees without earned income, but the Foreign Tax Credit might.

- Double Taxation Treaties: Some countries (like Portugal or Germany) have tax treaties that may help avoid paying tax twice.

- Capital Gains: Selling U.S.-based assets abroad may trigger unexpected tax events. Always consult a cross-border tax advisor.

💳 Banking and Currency Risk

- Open local bank accounts for easier bill payments and transfers.

- Use TransferWise (Wise) or Revolut to exchange money at better rates than traditional banks.

- Currency fluctuation can affect your purchasing power. Consider holding some local currency and using multi-currency accounts.

📄 Residency Rules

- Most countries require a retirement visa, proving income or savings.

- Some countries (e.g. Mexico, Georgia) allow long stays with easy renewals.

- A few offer investment-based permanent residency, such as Portugal’s Golden Visa or Panama’s Friendly Nations Visa.

✅ Pro Tip: Don’t assume your destination has the same paperwork standards or timelines as your home country. Get professional help if needed.

Healthcare: Will You Be Covered?

Healthcare is the top concern for retirees — and one of the best reasons to move abroad.

Countries with Strong Public and Private Options:

- Portugal: Public system is free/low cost; many retirees add private insurance.

- Mexico & Thailand: Private care is excellent and much cheaper than in the U.S.

- Costa Rica: Public care via the Caja, or high-end private hospitals in San José.

- Georgia: Basic public care; good private clinics for expats.

🩺 Expect to pay $100–$300/month for private insurance in most countries, or even less with local plans.

💡 U.S. Medicare does not cover services outside the U.S. You’ll need international insurance, self-pay, or access to local plans.

Hidden Costs of Retiring Abroad

While retiring abroad offers major savings, there are costs many don’t factor in:

- ✈️ Annual Travel Home: Even one or two trips per year can cost $1,000–$2,000+ each.

- 📦 Shipping or Storage: Moving belongings can be expensive — many expats downsize drastically.

- 💼 Legal/Translation Fees: For residency paperwork, leases, or even marriage certificates.

- 🛂 Immigration Consultant Costs: Optional, but can simplify visa renewals or tax filings.

Budgeting for these up front will help avoid unpleasant surprises.

Sample Monthly Budget in Mexico, Portugal, and Thailand (2025 Estimates)

| Expense | Mexico | Portugal | Thailand |

| Rent (1BR apartment) | $600 | $800 | $500 |

| Utilities & Internet | $100 | $120 | $100 |

| Groceries | $250 | $300 | $200 |

| Private Insurance | $150 | $180 | $120 |

| Transport & Dining | $200 | $250 | $150 |

| Total | $1,300 | $1,650 | $1,070 |

As you can see, even in Europe, it’s possible to live well under $2,000/month.

Emotional and Social Factors to Consider

Retiring abroad isn’t just about money — it’s a major life transition that can affect your emotional well-being in unexpected ways.

🏠 Loneliness and Isolation

- Moving away from familiar environments, family, and social circles can lead to feelings of loneliness — especially after the initial excitement fades.

- Language barriers and cultural differences can make it harder to form close relationships or integrate into local communities.

💡 Tip: Choose locations with expat networks or active retirement communities. Facebook groups, Meetup events, and international clubs can help bridge the gap.

🌐 Language and Communication

- Even in English-friendly countries, things like medical visits, legal documents, and local bureaucracy may only be in the native language.

- Learning basic local phrases is not just respectful — it can ease your daily life tremendously.

- Some countries (e.g. Portugal, Georgia, and parts of Mexico) offer language classes specifically for expats.

🧠 Cultural Adaptation

- Everyday routines, customer service, punctuality, and even social etiquette may feel unfamiliar or frustrating at first.

- Successful retirees abroad are flexible, curious, and open-minded — seeing challenges as part of the adventure.

✅ Ask yourself: Are you okay with slower bureaucracies? Will you miss certain foods or traditions? Are you comfortable not always being in control?

👨👩👧👦 Family and Grandchildren

- Many expats report feeling distant from children or grandchildren left behind.

- Time zones and travel costs can limit visits.

- Having a plan — such as yearly visits or part-year stays in your home country — can ease this emotional gap.

Technology Can Bridge the Distance

The good news? In 2025, tech makes retirement abroad more seamless than ever.

- 📲 Banking & Bill Pay: All manageable online.

- 💬 Communication: WhatsApp, Zoom, and FaceTime keep families close.

- 👩⚕️ Telemedicine: Many expats now use U.S.-based or global virtual doctors.

- 🛒 Shopping: Amazon and local e-commerce services cover most needs.

Even if you move thousands of miles away, you’re never fully disconnected — unless you want to be.

Top Mistakes to Avoid When Retiring Abroad

Even with thorough planning, many retirees fall into the same traps. Avoiding these common mistakes can save you serious stress and money.

1. Underestimating Total Costs

- Many people move abroad for lower living costs — but forget to account for:

- International health insurance

- Unexpected travel (e.g. emergencies back home)

- Currency fluctuations

- Import taxes on personal goods

- Always pad your monthly budget with a 15–20% buffer.

Important to not underestimate costs and to not overestimate your assets to retire. As you can see, with lower amount of money retiring in richer countries is hardly an option.

2. Not Testing the Waters First

- Moving sight unseen is risky. Spending 2–6 months living in your desired country — not just vacationing — helps reveal the day-to-day reality.

- Use this “test run” to explore housing, health care, local services, and expat communities.

3. Failing to Understand Residency Rules

- Some countries allow long stays visa-free; others require income proof, health insurance, or police checks.

- Applying for the wrong visa (or overstaying) can lead to hefty fines or bans.

- Each country’s rules differ — always consult a relocation advisor or local immigration lawyer.

4. Assuming You’ll Never Move Again

- Some retirees treat relocation as “forever” — but life changes. Health issues, family needs, or rising costs may prompt a return.

- Keep some financial flexibility, and don’t burn all bridges back home.

5. Overcomplicating Finances

- Juggling multiple bank accounts, currencies, tax systems, and retirement accounts across borders is no joke.

- Consider:

- Consolidating accounts where possible

- Using international-friendly banks

- Consulting a cross-border financial advisor or CPA

Final Thoughts: Is Retiring Abroad the Right Move for You?

Retiring abroad in 2025–2027 can unlock a lifestyle of adventure, affordability, and renewal — but only for those who plan wisely.

For some, it’s about stretching a modest retirement fund further. For others, it’s about climate, culture, or escaping domestic stressors. But whether you’re considering Mexico, Portugal, Thailand, or somewhere more remote, remember: retiring abroad is as much a financial decision as it is an emotional one.

To succeed, focus on:

- Affordability and cost of living — don’t just chase cheap rent; calculate total expenses.

- Healthcare access and quality — aging abroad without a plan can be risky.

- Currency risk and income logistics — inflation and exchange rates can erode your money.

- Visa, tax, and legal compliance — small paperwork mistakes can ruin your plans.

- Cultural fit and community — your happiness abroad depends on more than money.

Most importantly: don’t go it alone. Connect with expat groups, local advisors, and financial experts who understand your chosen country. Spend time on the ground. Test the waters before diving in.

Retirement is not just the end of a career — it’s the start of a new life chapter. With careful preparation, retiring abroad could be the most rewarding move you’ll ever make.