As living costs in the U.S., Canada, and parts of Europe continue to rise, many future retirees are asking a critical question:

Can I realistically retire abroad with $500,000 in savings?

The answer is yes — but with major caveats. Half a million dollars can go a long way in the right country with the right plan. But without understanding local costs, visa rules, taxes, and healthcare logistics, your dream retirement can quickly become a stressful money drain.

In this article, we’ll break down:

- What $500k means abroad in 2025–2027

- Where it works best (and where it doesn’t)

- How to avoid the most common traps

- Real budgeting strategies to stretch your savings for 20+ years

What $500,000 Gets You Abroad (in Today’s Money)

If you think $500k isn’t much in New York or London — you’re right. But in countries with much lower living costs and favorable exchange rates, it can support a comfortable, often luxurious lifestyle.

Let’s define a few spending categories:

| Lifestyle Level | Approx. Monthly Spend | $500k Duration |

| Frugal expat | $1,200 – $1,500 | 25–30+ years |

| Comfortable living | $2,000 – $2,500 | 18–22 years |

| Luxury expat | $3,000 – $4,000 | 10–14 years |

Key assumption: No rental income, no part-time work, no Social Security. Just drawing from savings (adjusted for ~3% annual inflation).

Countries Where $500k Works Very Well

These countries combine low costs, high safety, and generally welcoming visa systems for retirees:

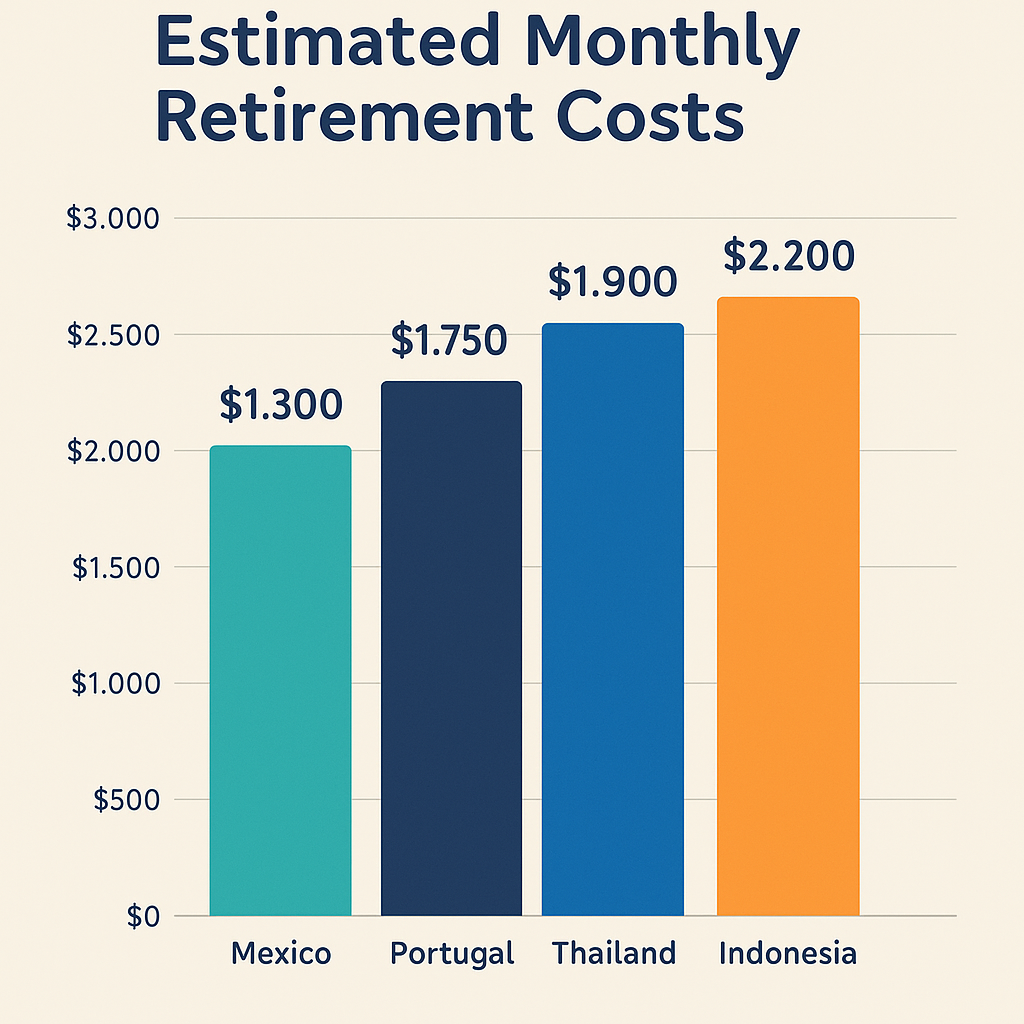

- Portugal

- EU healthcare access (with residency)

- $2,000–$2,500/month for comfortable lifestyle

- Non-Habitual Resident (NHR) tax incentives (phasing out but still useful)

- Mexico

- Proximity to U.S.

- Excellent private healthcare for affordable rates

- $1,500–$2,200/month in many cities

- Costa Rica

- Pensionado visa available

- Natural beauty + stable democracy

- $1,800–$2,500/month with private health options

- Thailand

- Long-stay retirement visa available

- Healthcare ranked among best in Asia

- $1,200–$2,000/month can buy a lot in Chiang Mai, Hua Hin, or parts of Bangkok

- Colombia or Ecuador

- $1,200–$1,800/month = very comfortable life

- Residency options for retirees

- Vibrant expat communities in Medellín and Cuenca

Where $500k Might Not Be Enough (Without Supplemental Income)

- Western Europe (France, Germany, Ireland): Higher rent, insurance, taxes.

- United States (as a foreign retiree): Healthcare costs, housing, and visa inaccessibility.

- Japan & South Korea: Higher cost of living and more complex visa paths.

- Popular Cities (Lisbon, Barcelona, Bali now): Gentrification + inflation are raising costs quickly.

Even some “cheap” destinations are now pricing out long-term retirees. Research city-specific data — not just country-level averages.

How to Avoid the Most Common Mistakes

- Underestimating Healthcare Costs

- Private health insurance for expats can range from $50/month (Asia) to $500/month (Europe)

- Not all countries accept Medicare or cover pre-existing conditions

- Ignoring Currency Risk

- Your U.S. dollars may lose value if local currency strengthens

- Consider multi-currency accounts or investing in local currency assets

- Forgetting Tax Reporting

- U.S. citizens must file taxes worldwide (even with $0 owed)

- Some countries tax global income. Use tax treaties smartly.

- Failing to Establish Residency

- You need a visa or residency permit — tourist visas won’t work long term

- Some countries require proof of income (e.g., $2,000/month minimum)

- Overestimating Rental Income

- Planning to rent out your U.S. house while living abroad?

- That income is not guaranteed. Markets shift. Tenants default. Always have a Plan B.

How to Stretch $500,000 for a 20+ Year Retirement Abroad

Even in a low-cost country, careful planning is key to make your nest egg last. Here’s how smart expats make $500,000 work for decades:

1. Rent Smart — or Buy Strategically

- Renting gives flexibility and protects you from real estate scams or local legal traps. Avoid buying in your first 12–24 months abroad.

- Buying may make sense in stable markets like Portugal or Mexico, especially outside major cities. But factor in property taxes, maintenance, HOA fees, and legal costs.

- Avoid tourist traps and opt for 2nd-tier cities or rural coastal zones, where rent is often 30–50% cheaper.

Tip: Spending $600–$900/month on rent in a walkable, safe area can save you over $150,000 across 20 years compared to Western cities.

2. Use Local Health Systems — Not Global Insurers

- Many countries offer quality public or semi-private health care for residents. In places like Thailand or Colombia, private healthcare is excellent and affordable.

- Global expat health insurance can cost over $5,000/year — and may not be worth it for healthy retirees under 70.

- Explore local health plans once you gain residency. In Portugal, for example, once a resident, you’re covered under the SNS system.

3. Supplement Income with Remote or Passive Work

Even $500–$1,000/month from:

- Freelance writing or consulting

- Teaching English online

- Managing U.S.-based rental income

- Running a YouTube or Substack channel

…can extend your retirement timeline by 5–10 years. It also gives you flexibility to handle emergencies without dipping into capital.

4. Keep Emergency and Relocation Funds Separate

Don’t count every dollar of your $500k as spendable. Set aside:

- $15,000–$25,000 as emergency reserve (medical, family issues, evacuation)

- $5,000–$10,000 for potential relocation (visa problems, local political unrest, personal dissatisfaction)

Peace of mind = priceless.

5. Diversify Currency and Bank Holdings

Keep your money across 2–3 currencies or countries:

- A U.S. account for Social Security, brokerage access

- A local account for monthly expenses

- Possibly a Euro or Swiss account for stability

This protects you from bank freezes, FX crashes, or capital controls — all of which have happened in the last decade.

6. Adjust Spending with Inflation and Markets

Prices will rise. Some years your portfolio may drop 10–20%. Plan for flexibility:

- If markets are down, reduce monthly draws

- Avoid inflation-heavy areas (e.g., rental bubbles in Bali or Lisbon)

- Stay nimble — if costs rise too much, be willing to relocate to a cheaper city or country

Where to Live Tax-Wise: Minimizing Taxes on a $500,000 Retirement

One of the smartest ways to stretch your savings is to minimize taxes — legally — in retirement. Here’s how:

1. Choose Tax-Friendly Countries for Foreigners

Some countries don’t tax foreign income, including:

- Panama: No tax on foreign-earned income; territorial system.

- Costa Rica: Foreign retirement or investment income generally not taxed.

- Malaysia: No tax on foreign-source income remitted into the country (as of 2025).

- Georgia and Paraguay: Very low tax rates and no foreign income tax.

Portugal’s NHR program (Non-Habitual Residency) previously offered 10 years of low taxation on pensions but is being phased out — stay up to date.

2. Understand U.S. Tax Implications

Even if you live abroad, U.S. citizens must file taxes each year. But you may benefit from:

- Foreign Earned Income Exclusion (FEIE): Excludes ~$120,000/year of earned income (not pensions or investments).

- Foreign Tax Credit: If you pay tax abroad, you can offset U.S. taxes.

- Treaties: Some countries have U.S. tax treaties that prevent double taxation of Social Security or pensions.

Important: Roth IRA withdrawals are tax-free in the U.S. — and often ignored abroad — making them powerful for expat retirees.

3. Use a Retirement Drawdown Strategy

Structure your withdrawals for efficiency:

- Tap taxable brokerage accounts first

- Delay Social Security if possible to maximize monthly payments

- Use Roth IRA or Roth 401(k) last, to keep tax-free growth going

- Consider converting traditional IRAs to Roths during low-income years abroad

This layering approach helps avoid high tax brackets and preserves capital longer.

How to Handle Rising Costs in 2030s and Beyond

Retiring on $500k in 2025 is realistic in many countries — but what about 10 or 20 years from now?

Here’s how to future-proof your plan:

- Expect 3–5% inflation annually in many developing countries (possibly more in Asia and Latin America).

- Build a margin of safety: If your budget is $2,000/month, plan as if it’s $2,500/month by 2035.

- Use local investments or rental income to match future local expenses.

- Consider countries with strong infrastructure and currency to weather inflation better (Portugal, Chile, Poland).

Building a Resilient Retirement Plan Abroad on $500K

Beyond just selecting a country and budgeting carefully, a successful retirement abroad requires layered preparation in three key areas: healthcare, legal status, and contingency planning.

1. Healthcare: Quality, Insurance, and Emergencies

- Private Healthcare Abroad: Many developing nations offer excellent private care at a fraction of U.S. prices. For example, expats in Thailand, Mexico, Portugal, and Turkey regularly report high satisfaction with private hospitals and doctors.

- Health Insurance: International health insurance plans range from $1,500–$3,500 per year per person depending on coverage and age. Some expats use local private insurance instead, which can be as low as $50–$100/month.

- Emergency Planning: Consider:

- Will you need to fly back to the U.S. for treatment?

- Are you close to a major hospital?

- Will your care be in English, or will you need a translator?

Pro Tip: Keep at least $10,000 in liquid emergency funds for unexpected medical needs or evacuation.

2. Legal Residency and Visas

Retiring abroad requires more than just showing up:

- Retirement Visa Programs: Countries like Panama, Thailand, Mexico, and Portugal have dedicated retiree visas. Most require proof of income (e.g., $1,500–$2,500/month) or savings.

- Permanent Residency vs. Long-Term Visa: PR often allows more rights and lower restrictions, but takes time. For short-term stays, renewable 1–5 year visas are easier.

- Citizenship by Investment/Residency: If you plan to stay forever, countries like Paraguay, Malta, or Turkey may offer accelerated paths through investment or property purchase.

Make sure you consult a local immigration lawyer before finalizing your plans.

3. Contingency Plans: What If Life Changes?

Retirement is rarely a straight line. Here’s how to stay flexible:

- Exit Strategy: What if local laws change? Or healthcare declines? Keep enough funds for a relocation, ideally to a second option on your list.

- Currency Fluctuations: If local currency collapses (as seen in Argentina, Turkey), it can inflate your costs overnight. Keep some savings in USD, EUR, or gold-linked assets as a hedge.

- Family and Social Ties: Consider the emotional cost of distance. Some retirees return after a few years because they feel isolated. Choosing an expat-friendly community helps ease transition.

- Digital Access: Set up remote banking, bill pay, and tax filing. You’ll need to manage your finances internationally.

Can You Retire Abroad on $500K Comfortably?

Yes — if you choose the right country, budget realistically, and plan thoroughly, $500,000 can last 20+ years abroad. But it requires:

- Low cost of living destination (ideally $1,500–$2,000/month total expenses)

- Wise investment strategy to keep pace with inflation

- Flexibility, discipline, and clear backup plans

In many parts of the world, a modest nest egg goes much further than you think. But you must approach it like a strategic life relocation, not just a vacation.

Final Thoughts: Is Retiring Abroad on $500,000 Realistic?

Retiring abroad with $500,000 isn’t a fantasy—it’s a well-documented path that thousands of Americans and Europeans are taking each year. But it’s not without its challenges. Success depends on:

- Where you go: A country’s cost of living, visa rules, healthcare system, and safety make a huge difference.

- How you plan: Budgeting, insurance, legal status, and emergency backup plans are crucial.

- How flexible you are: Markets change, rules evolve, and life throws curveballs—especially when living internationally.

The good news? With proper planning, $500K can fund a fulfilling, comfortable retirement in places where your money stretches much further. You may even afford a better lifestyle than back home—think ocean views, vibrant markets, affordable healthcare, and a slower pace of life.

But this path is best for adventurous, independent retirees who value experience over luxury, and are willing to adapt to a new culture.

Bottom line: For the right person in the right country, retiring abroad on $500,000 isn’t just possible—it might be the best decision you ever make.