A realistic breakdown for 2025–2027 retirees navigating inflation, market volatility, and rising life expectancy

Introduction: The $1 Million Question

For decades, $1 million was considered the gold standard of retirement security — a psychological milestone that promised peace of mind and financial independence. But in 2025, with rising inflation, healthcare costs, and longer lifespans, many near-retirees are asking a sobering question:

Is $1 million still enough to retire at 65 — and stay retired comfortably?

This article breaks down what $1 million really means in today’s financial climate. We’ll look at:

- Safe withdrawal strategies

- Longevity risk and lifestyle inflation

- What $1M actually buys today in housing, healthcare, and travel

- And whether alternatives like gold, crypto, or dividend stocks can help extend your nest egg

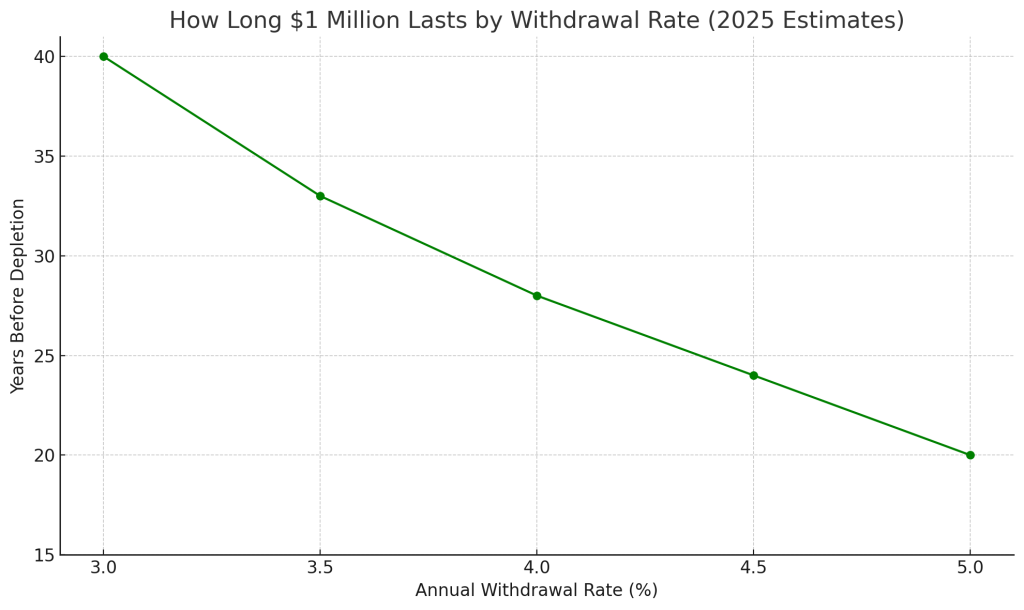

Part 1: How Long Can $1 Million Last in 2025?

Let’s start with the math. The rule of thumb for retirement withdrawals has long been the 4% rule, meaning you withdraw 4% of your savings each year and increase it with inflation.

Under the 4% rule:

- Annual withdrawal = $40,000/year

- Retirement length covered = 25–30 years (based on historic averages)

But 2025 is not average.

Real-World Pressures on Your $1M:

| Factor | Impact |

| Inflation (3.5–4.5%) | Reduces your purchasing power over time |

| Bond yields (still low) | Difficult to get safe income > 4% without risk |

| Healthcare inflation | Costs rising faster than CPI, especially after age 70 |

| Longevity risk | Many retirees live past 90 — even 95 |

That means $40,000/year may not go as far in 2035 as it does in 2025 — and if markets underperform, you risk drawing down too quickly.

Part 2: Adjusting Withdrawal Strategy — The 3% Rule?

Some advisors in 2025–2026 are now recommending a 3.3% withdrawal rate (not 4%) to protect against sequence-of-returns risk.

What does that mean?

- Withdraw just $33,000/year from $1 million

- Potentially stretches your retirement horizon to 30+ years, even through downturns

- Less strain during bear markets or high inflation periods

Key Consideration:

The earlier you retire, the lower your safe withdrawal rate should be — especially if you won’t receive full Social Security until age 67–70.

Let me know when to continue with:

- Part 3: What $1 Million Buys in 2025 – Housing, Healthcare, Lifestyle

- Part 4: Stretching $1M with Gold, Crypto, or Income Investments

CHART How Long $1 Million Lasts by Withdrawal Rate (2025 Estimates)

Part 3: What $1 Million Really Buys in 2025

Even if you follow a conservative withdrawal strategy, the real test of retirement success is what that money can buy you. And in 2025, prices for essentials — especially housing and healthcare — have shifted dramatically in many regions.

Housing: Rent or Own in Retirement?

If you already own your home outright, congratulations — that’s one of the best inflation hedges you could have. But if you’re still renting or planning to downsize, here’s what $1 million looks like:

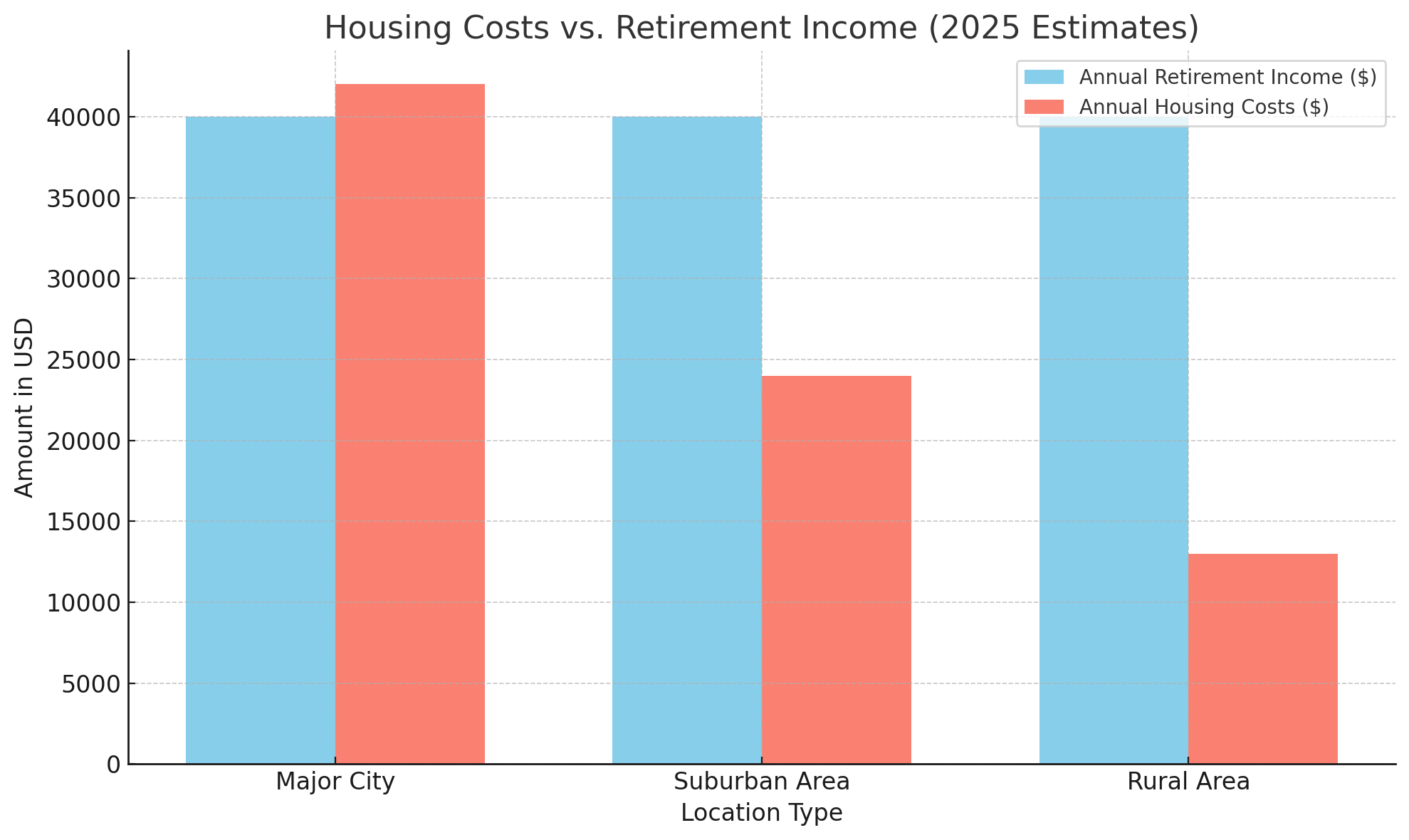

| Location Type | Monthly Rent (1BR–2BR, mid-range) | Annual Housing Cost |

| Major City (NY, LA) | $2,500–$3,800 | $30,000–$45,600 |

| Suburbs / Small City | $1,600–$2,200 | $19,200–$26,400 |

| Rural / Low-Cost | $900–$1,400 | $10,800–$16,800 |

➡ If your annual retirement budget is ~$40,000 (based on 4% withdrawal), housing alone can consume 50–75% in some cities.

And don’t forget: property taxes, home repairs, and rising insurance premiums (especially in flood/fire-prone states) can chip away at your reserves.

Healthcare: The Hidden Cost Multiplier

Healthcare is one of the biggest unknowns in retirement planning. According to Fidelity’s 2025 estimate, a 65-year-old couple retiring today will need around $345,000 for healthcare expenses over retirement — and that’s excluding long-term care.

Here’s how healthcare can impact your $1M nest egg:

| Cost Category | Annual Estimate (per person) |

| Medicare premiums | $2,000–$3,000 |

| Out-of-pocket copays | $1,000–$2,500 |

| Medications | $1,200–$3,000+ |

| Dental/vision/hearing | $800–$1,200 |

| Supplemental coverage | $2,000–$4,500 |

➡ A relatively healthy couple could still spend $10,000–$15,000 per year combined — 25–40% of your $40,000 annual draw.

And if you or your spouse develops a chronic illness or needs assisted living, that number could skyrocket.

Lifestyle: What Kind of Retirement Are You Really Buying?

Even with the basics covered, many retirees hope for more than just getting by — they want to travel, enjoy hobbies, and spend on family.

But let’s look at a few real-world retirement splurges in 2025:

| Item/Event | Typical Cost (USD) |

| 2-week Europe trip | $8,000–$12,000 per couple |

| Cruise (7–10 days) | $5,000–$7,500 |

| Golf club annual fees | $3,000–$10,000+ |

| Home renovation project | $20,000–$50,000 |

| Helping grandkids w/ college | $5,000–$20,000+ |

That’s why many retirees with $1M still worry — there’s little room for error or spontaneity.

Part 4: How to Stretch $1M with Smart Assets — Gold, Crypto, and Dividends

A $1 million portfolio can provide security, but it rarely offers comfort without smart positioning. The key is protecting principal while also generating income or inflation-adjusted growth.

Let’s look at how some asset classes can help stretch your $1 million — or possibly backfire if misused.

Gold: Reliable Hedge or Dead Weight?

Gold has long been viewed as a safe haven — and rightly so. Since the 1970s, gold has protected purchasing power during inflationary and crisis periods.

In 2025, gold is trading at or near $3,400/oz, up sharply since 2020. But should retirees hold it?

| Gold Pros | Gold Cons |

| Inflation hedge | No yield (produces no income) |

| Crisis protection | Can underperform in bull markets |

| Diversifies away from equities | Hard to rebalance without selling |

🔹 Recommended allocation: 5–15% of portfolio (especially if nervous about U.S. debt, inflation, or geopolitics)

₿ Crypto: Growth Engine or Volatile Gamble?

Bitcoin has outperformed every asset class over the past 10 years — including stocks, gold, and real estate. But that came with stomach-churning volatility. In 2022, Bitcoin fell over 70%, before recovering to new highs in 2025 near $110,000.

Can retirees use it? Carefully.

| Crypto Use Case | Retirement Viability |

| Long-term capital growth | ✅ Hold 1–5% for upside |

| Inflation hedge (vs. fiat) | ⚠️ Unproven during recessions |

| Daily income generation | ❌ Highly unreliable |

Crypto ETFs (like spot Bitcoin ETFs) can offer easier access, but most advisors limit crypto to a speculative sleeve of your portfolio — not the core.

Dividend Stocks: Yield + Growth

Unlike gold or Bitcoin, dividend-paying stocks offer something unique: ongoing income with the potential for capital appreciation.

Many retirees in 2025 are turning to:

- Dividend Aristocrats (25+ years of increasing dividends)

- REITs (Real Estate Investment Trusts)

- Utilities and energy pipelines with stable yields

| Asset Type | Typical Yield (2025) |

| Dividend ETFs (VIG, SCHD) | 2.0%–3.5% |

| REITs (VNQ, O) | 4.0%–6.0% |

| Blue-chip utilities | 3.5%–4.5% |

A $1M portfolio with 3.5% dividend yield = $35,000/year in passive income — with principal potentially growing over time.

Final Thoughts: Yes, But Only with a Plan

So… is $1 million enough to retire at 65?

✅ Yes — if you:

- Keep expenses in check

- Withdraw at 3–4%

- Use diversified, income-generating assets

- Plan for inflation and healthcare surprises

🚫 No — if you:

- Expect luxury travel every year

- Have no plan for medical costs

- Rely only on cash or bonds

- Retire early without Social Security

Ultimately, the real answer is: It depends on your lifestyle, asset mix, and how you respond to risk.

Part 5: Social Security and Supplemental Income — A Crucial Lifeline

For many Americans, Social Security remains a cornerstone of retirement income. If you’re retiring at 65 in 2025, your full retirement age (FRA) under current law is 66 years and 10 months. Retiring a few months early may reduce your monthly benefits, but those benefits can still meaningfully supplement a $1 million nest egg.

Average Social Security benefit at age 65 in 2025:

- Around $2,050–$2,300 per month, or $25,000–$28,000 annually

If you and your spouse both qualify, that’s potentially $50,000–$55,000/year in Social Security income — which can double your budget if your withdrawals from savings are around $40,000/year.

Social Security also comes with cost-of-living adjustments (COLA), which help keep up with inflation, something many private pensions do not offer. The 2025 COLA increase was 3.2%, following 8.7% in 2023 and 5.9% in 2022.

However, if you plan to rely heavily on Social Security:

- Consider delaying benefits to age 67 or 70 for maximum payouts

- Monitor legislative changes, as reforms may reduce benefits in the 2030s

Combined with modest withdrawals and a conservative portfolio, Social Security may help keep your retirement plan viable for 30+ years — even with market bumps along the way.

Part 6: Real-Life Retirement Scenarios with $1 Million

Let’s take three hypothetical examples to bring these numbers to life.

Scenario A: Suburban Conservative

- 65-year-old homeowner in Ohio

- Spends modestly: $35,000/year

- Draws $25,000 from Social Security, $10,000 from savings

- Invested in 60/40 portfolio with 5% gold

- Likely to outlive savings with a cushion

Scenario B: Urban Spender

- 65-year-old renting in Los Angeles

- Spends $60,000/year on housing, travel, lifestyle

- Pulls $32,000 from Social Security, $28,000 from portfolio (2.8%)

- High exposure to growth stocks and some crypto

- At risk if markets underperform or inflation spikes

Scenario C: Flexible Retiree with Side Income

- 65-year-old in Florida with paid-off home

- Works part-time earning $12,000/year

- Draws $20,000/year from savings, $24,000 Social Security

- Keeps 30% in dividend ETFs and 10% in gold

- Balanced, diversified, and likely to succeed long term

What separates success from failure isn’t just the total dollar amount, but how that money is structured, protected, and used strategically.

Conclusion: $1 Million Can Work — If You Respect Its Limits

In today’s economic reality, $1 million is no longer a magic number. It’s a strong starting point, but not a guarantee of lifelong financial freedom. For someone retiring at 65 in 2025–2027, that sum can cover 25–30 years of modest living — but it must be managed with care.

The key takeaways:

- Inflation, healthcare, and longevity risk can erode purchasing power faster than you think

- A withdrawal strategy under 4%, ideally closer to 3.3%, is now considered safer

- Mixing traditional assets with dividends, gold, and (optionally) crypto can enhance durability

- Social Security can significantly extend your runway — especially if delayed

- The lifestyle you choose matters more than the savings total

If you’re entering retirement with $1 million, think of it as a well-stocked ship, not an invincible fortress. With the right map and a steady hand on the wheel, it may carry you safely to shore.