In 2025, the idea of retiring with Bitcoin is no longer a fringe fantasy. With institutional adoption rising, spot ETFs approved, and more investors holding BTC for the long haul, the question isn’t “Is it possible?” but rather “How should you actually do it?”

This guide breaks down the realistic strategies, risks, and numbers for anyone considering Bitcoin as part of their retirement plan — whether you’re 30, 45, or even 60+.

Why Bitcoin May Belong in a Retirement Portfolio

Bitcoin was once viewed as a speculative gamble. Today, it’s evolving into a macro asset, often compared to gold or even real estate — but with higher upside (and volatility).

Here’s why retirement planners and financial advisors are starting to take it seriously:

- Hard-capped supply: Only 21 million BTC will ever exist — a built-in inflation hedge

- High long-term returns: Despite crashes, BTC has outperformed nearly every asset class over 10+ years

- Digital native: Borderless, portable, and increasingly accessible via mainstream brokers and retirement platforms

- Growing institutional interest: Pension funds and endowments are now quietly adding exposure

If you believe that Bitcoin will continue maturing as a store of value, including it in a retirement plan becomes not just viable — but strategic.

Who Should Consider Retiring with Bitcoin?

Retiring with Bitcoin doesn’t mean betting your entire future on it. It means including BTC as part of a broader retirement mix — to boost potential returns, hedge fiat risk, or diversify out of legacy assets.

You might consider a Bitcoin-inclusive retirement strategy if:

- You’re under 50, with time to recover from short-term volatility

- You already own traditional retirement assets (401(k), IRA, stocks)

- You’re open to self-directed investing or using crypto IRAs

- You believe in Bitcoin’s long-term relevance, even if not short-term performance

But even older investors (55+) are now using BTC as a small hedge or long-term inheritance strategy — especially those concerned about fiat devaluation or systemic financial risk.

The Risks of Relying on Bitcoin Alone

Before we dive into strategy, let’s get real:

Bitcoin is not a magic retirement bullet. It comes with serious risks, including:

- Extreme volatility — 50–80% drawdowns happen regularly

- Regulatory uncertainty — Especially outside the U.S.

- Security risks — Loss of private keys = permanent loss

- No cash flow — Unlike dividend stocks or rental property, BTC doesn’t generate income

Even Bitcoin’s strongest advocates admit it should not be 100% of your retirement portfolio. Rather, it’s best treated as a high-risk, high-reward layer — like early-stage tech stocks were in the 1990s.

Realistic Bitcoin Retirement Scenarios: What Could It Look Like?

Scenario 1: Retiring with $100,000 in Bitcoin

Let’s say you accumulated $100,000 in BTC by 2025. What could that mean for retirement?

Best-case outcome (BTC grows to $250K):

- Your BTC value grows 2.3× to ~$230,000 by 2030

- If paired with other assets (cash, gold, or rental income), this could provide modest supplemental income for a lean retirement

- But if Bitcoin stagnates or drops, you may be forced to work longer or draw from other accounts

Realistic approach:

- Keep BTC as a growth layer, but ensure 60–70% of your savings are in low-volatility assets

- Plan to draw only 4–6% annually from BTC unless major gains are realized

Bottom line: $100K in BTC alone won’t secure retirement — but it could meaningfully extend the life of your other savings.

Scenario 2: Retiring with $300,000 in Bitcoin

Now we’re talking. With $300K in BTC, you have a true long-term asset base — but also more at stake if markets crash.

Balanced strategy:

| Allocation | Notes |

| 50% BTC ($150K) | Long-term HODL; consider cold storage |

| 25% Gold/Cash ($75K) | Volatility buffer for bear markets |

| 25% Equities/Bonds ($75K) | For income generation or dividend reinvestment |

This portfolio gives you upside potential while protecting capital during market downturns.

Withdrawal strategy:

- Use BTC only when price exceeds targets (e.g., $150K+)

- Otherwise, draw from cash/gold in down cycles

Optional upgrade: Allocate some BTC to interest-earning crypto accounts, but only on trusted platforms (and not more than 10–15%).

Scenario 3: Retiring with $1 Million+ in Bitcoin

At this level, Bitcoin becomes not just a retirement asset — but a generational wealth vehicle.

Two primary approaches:

- Preservation-focused

- Move at least 50–70% to cold storage

- Keep 10–20% in liquidity for living expenses

- Allocate 10% to income-generating products (e.g., stablecoin staking, covered call strategies)

- Growth hybrid

- Use BTC as a base

- Layer with gold, dividend ETFs, and a small cash flow business

- Use Bitcoin volatility to “rebalance” other assets (buy dips, sell rips)

At this tier, you may also want a trust or estate plan involving Bitcoin, especially if heirs are not crypto-savvy.

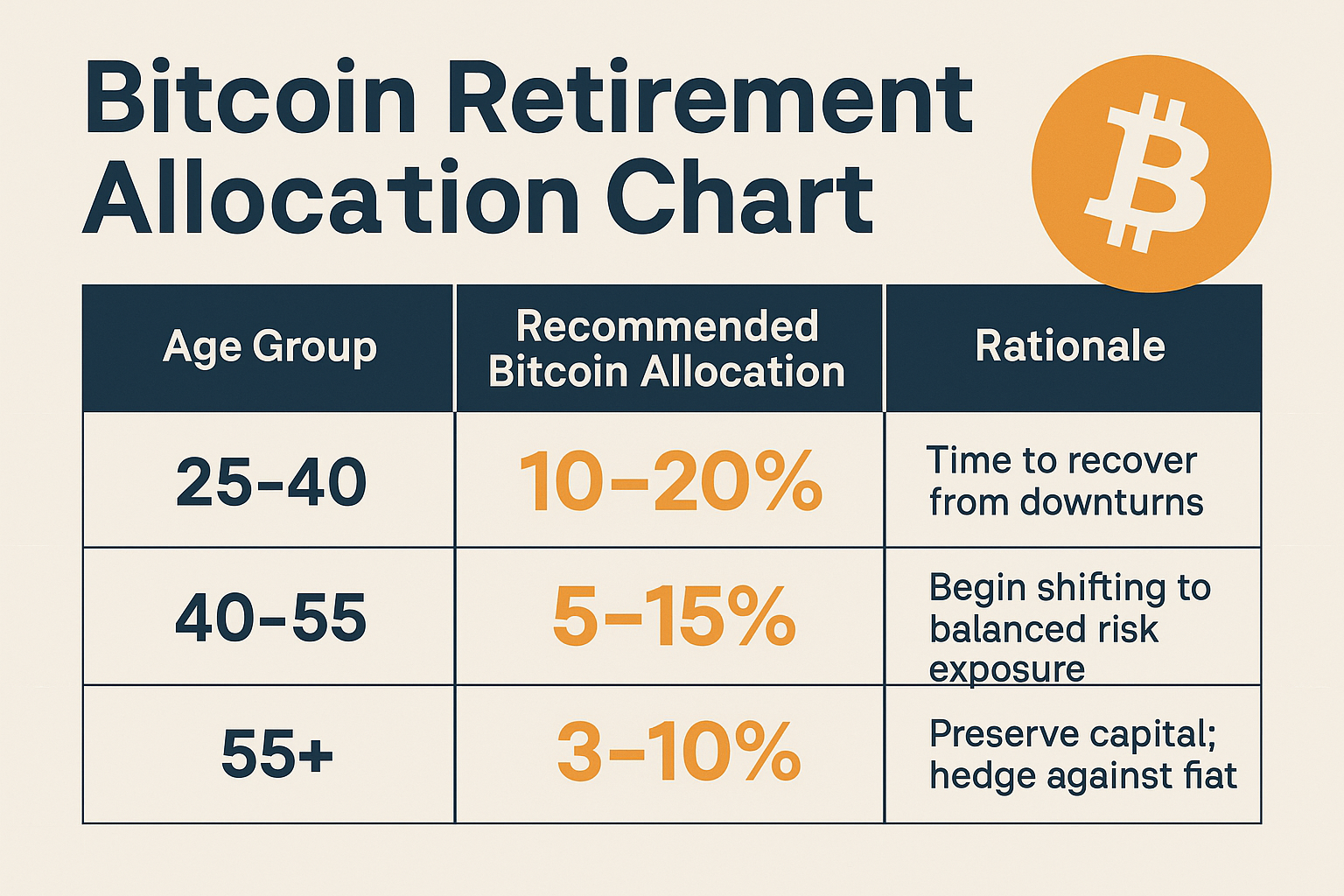

How Much Bitcoin Should Be in a Retirement Portfolio?

There’s no universal answer — but most credible advisors suggest a 5% to 20% allocation, depending on age, risk tolerance, and wealth level.

| Age Group | Recommended BTC Allocation | Rationale |

| 25–40 | 10–20% | Time to recover from downturns |

| 40–55 | 5–15% | Begin shifting to balanced risk exposure |

| 55+ | 3–10% | Preserve capital; hedge against fiat |

The key is to avoid overexposure. Bitcoin is powerful — but it should amplify, not dominate, your retirement plan.

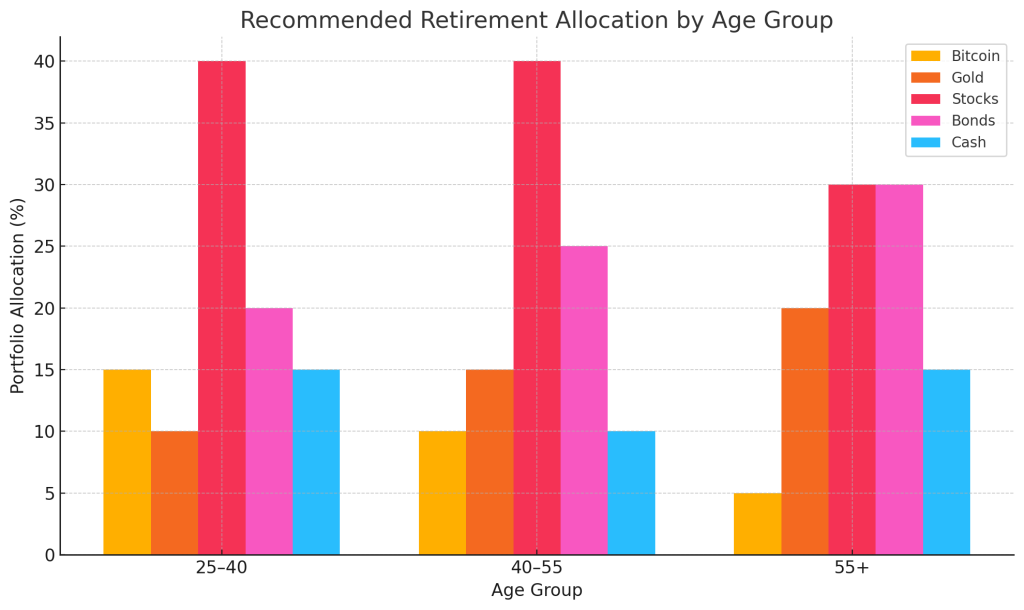

Building a Hybrid Retirement Portfolio: BTC + Traditional Assets

Here’s an example hybrid portfolio structure for 2025–2030:

| Asset Class | Suggested Allocation | Role in Portfolio |

| Bitcoin (BTC) | 10–20% | Growth, hedge vs. fiat debasement |

| Gold | 10–15% | Store of value, low correlation |

| Stocks (ETFs) | 30–40% | Growth + income through dividends |

| Bonds/CDs | 10–20% | Stability, predictable yield |

| Cash/Stables | 10–15% | Liquidity, crash protection |

This mix ensures you’re not overly reliant on BTC price swings — but can still benefit if Bitcoin outperforms.

Crypto Retirement Accounts: What Are Your Options?

In 2025, retiring with Bitcoin has become more accessible thanks to a range of new crypto-integrated retirement accounts. These options allow you to hold BTC (and sometimes ETH or stablecoins) within tax-advantaged structures, like IRAs or 401(k)s.

1. Self-Directed IRA (SDIRA)

This is the most flexible option for crypto retirement investing.

- You control the asset selection, including Bitcoin, Ethereum, and even tokenized real estate

- Typically held via a custodian like iTrustCapital, BitIRA, or Alto CryptoIRA

- Available in Roth or Traditional formats (tax now vs. tax later)

Pros:

- Tax-deferred (or tax-free) Bitcoin gains

- Option to diversify across multiple crypto assets

- Long-term cold storage available via custodians

Cons:

- Higher fees than standard IRAs

- Custody is not fully self-managed

- Requires paperwork and extra security steps

2. Crypto 401(k) Integration

Some fintech providers now let you allocate a portion of your 401(k) contributions to Bitcoin.

- Fidelity, ForUsAll, and other platforms offer this through employer-linked accounts

- Typically capped (e.g., max 20% in BTC), with Bitcoin held in institutional custody

- Great for long-term DCA (dollar-cost averaging) via payroll

Pros:

- Seamless integration with traditional retirement savings

- Institutional-grade security

- Dollar-cost average without thinking about it

Cons:

- Limited control over how/when to withdraw BTC

- Plan may restrict which crypto assets are allowed

How to Withdraw from Bitcoin in Retirement

One of the biggest challenges in retiring with BTC isn’t just owning it — it’s drawing income from it while managing risk.

Here are a few withdrawal strategies that make sense in 2025–2030:

1. Threshold-Based Selling

Sell BTC only when price exceeds a predetermined target. For example:

- Sell 10% of holdings when BTC crosses $150K

- Sell another 10% at $180K

- Hold the rest for legacy/inheritance

This avoids emotional decisions and lets you capitalize on upside.

2. Time-Based Rebalancing

Withdraw a fixed % annually regardless of price — e.g., 4–5% of your portfolio each year. This is like the traditional “4% rule” applied to crypto.

Tip: Combine with traditional assets to smooth volatility.

3. Income Layering

Hold stablecoins (e.g., USDC or tokenized T-bills) that can earn yield, while BTC acts as reserve capital.

- Withdraw income from stables

- Refill with BTC only when price is favorable

This gives you monthly income without constantly touching BTC.

Managing Volatility in a Bitcoin Retirement Plan

Bitcoin’s volatility doesn’t go away just because you’re retired. That means you need buffers and counterweights built into your plan.

Here’s how to protect your quality of life:

1. Always Have 12–24 Months of Living Expenses in Cash or Stablecoins

This allows you to ride out bear markets without having to sell BTC at a loss.

2. Pair BTC with Gold

Gold tends to rise or hold flat during Bitcoin crashes, offering a psychological and financial anchor.

Example: In 2022, when BTC dropped over 70%, gold stayed above $1,800 most of the year.

3. Don’t Forget Health and Tax Costs

Crypto assets aren’t always easy to sell, especially in large amounts. Plan ahead for:

- Healthcare expenses

- Emergencies

- Unexpected tax liabilities from large crypto gains

Pro tip: Pre-sell a small amount of BTC during bull markets and keep it as a tax reserve.

Final Thoughts: Bitcoin Can Be Part of a Real Retirement Plan

Gone are the days when Bitcoin was just a tech experiment or a gamble. In 2025, it’s a maturing global asset — one that can absolutely be part of a serious retirement plan if handled with care.

The key is balance:

- Don’t bet everything on Bitcoin

- Don’t ignore its potential either

- Use Bitcoin to amplify your retirement — not define it

If you’re building toward 2030 and beyond, Bitcoin could be the growth engine your plan needs — as long as it’s supported by stability, planning, and patience.

Long-Term Strategy: From Retirement to Legacy Planning with Bitcoin

One of the overlooked strengths of Bitcoin as a retirement asset is its potential to extend beyond your own lifetime. As more high-net-worth individuals and early adopters age, Bitcoin is now being positioned not just as a retirement asset — but as part of intergenerational wealth strategies.

Why Bitcoin Is Inheritable

Unlike fiat currencies, pensions, or even traditional 401(k)s, Bitcoin can be transferred:

- Across borders

- Outside of banking systems

- Without delays from probate courts (if structured correctly)

- In a form that retains scarcity and long-term value

This makes it a uniquely powerful tool for legacy planning, especially for families who are financially literate and comfortable with digital assets.

Tools for Generational Bitcoin Planning

If you’re thinking long-term — not just about your retirement but about your children or heirs — here are tools and practices to consider:

1. Multi-Sig Wallets

Multi-signature wallets allow two or more keys to be required for moving funds. This is ideal for:

- Shared family accounts

- Setting up contingency access

- Avoiding loss from a single point of failure

You can even structure multi-sig wallets to require approval from a lawyer or trustee if needed.

2. Bitcoin Trusts and Estate Plans

Firms like Casa, Unchained Capital, and some legal advisors now offer Bitcoin-specific estate planning services.

With these tools, you can:

- Include BTC in wills or living trusts

- Establish clear custody instructions

- Prevent access disputes or legal limbo after death

Tip: Make sure at least one family member or legal contact understands how to use your wallets. Loss of access = permanent loss of wealth.

3. Insurance for Digital Assets

Some high-net-worth individuals now purchase crypto-specific insurance policies to cover loss or theft of keys. This adds peace of mind, especially if a large portion of retirement is held in BTC.

Bitcoin vs. Real Estate: A Fresh Comparison for Retirement

Real estate has traditionally been the go-to asset for retirement and wealth transfer — but Bitcoin offers some compelling advantages in certain scenarios:

| Feature | Real Estate | Bitcoin |

| Liquidity | Low – hard to sell fast | High – sell anytime on global markets |

| Portability | Fixed asset | Global, borderless |

| Maintenance costs | High (taxes, repairs, tenants) | None (digital asset) |

| Volatility | Low | High |

| Passive income | Possible (rental) | Possible (staking, lending, etc.) |

| Estate complexity | High (titles, taxes) | Moderate (with planning) |

The conclusion isn’t that Bitcoin replaces real estate — but that it offers an alternative retirement asset class with complementary strengths, especially for mobile, tech-savvy, or globally-minded individuals.

The Emotional Side: Staying Sane in a Bitcoin Retirement

Managing your own retirement is hard enough — adding a volatile asset like Bitcoin can create stress unless you have the right mindset.

Here’s what successful Bitcoin retirees do differently:

- They zoom out — watching the 4-year cycle, not the 4-day candles

- They set and forget — planning withdrawals around goals, not emotions

- They automate — DCA in, rebalance quarterly, review once per year

- They educate their heirs — so future generations don’t mismanage the wealth

Perhaps most importantly, they understand this truth:

Bitcoin is a long-term story. Wealth isn’t made from volatility — it’s made from staying in the game.

Related posts:

Is Bitcoin the New Retirement Plan? Why More Americans Over 40 Are Turning to Crypto in 2026

Is Bitcoin the New Retirement Plan? Why More Americans Over 40 Are Turning to Crypto in 2026

Bitcoin vs. Ethereum in 2025-2026: Which One Should You Own?

Bitcoin vs. Ethereum in 2025-2026: Which One Should You Own?

How to Invest During an Election Year: Stocks, Gold, Crypto, or Cash? (2026)

How to Invest During an Election Year: Stocks, Gold, Crypto, or Cash? (2026)

How to Rebuild Your Retirement in Your 50s: 2026–2027 Guide for Late Starters

How to Rebuild Your Retirement in Your 50s: 2026–2027 Guide for Late Starters