As retirement looms on the horizon for millions of Americans, many are questioning the conventional financial wisdom that once promised security through pensions, 401(k)s, and real estate. In 2026, a surprising trend is taking shape: more Americans over 40 are turning to Bitcoin as part of — or even the core of — their retirement plans.

What’s behind this dramatic shift, and is Bitcoin a viable retirement strategy or a speculative gamble?

Let’s break it down.

The Crisis of Confidence in Traditional Retirement Vehicles (continued)

The post-pandemic economy, inflation waves of 2022–2024, and the ongoing interest rate volatility in 2025 have left many middle-aged Americans disillusioned with traditional retirement paths.

401(k)s have lost their shine due to market instability, employer contribution cuts, and the reality that many people started saving too late. Social Security is under pressure, with headlines warning that trust fund reserves could run low by the 2030s. Even real estate — once seen as a dependable retirement nest egg — is now a mixed bag amid regional price bubbles and rising property taxes.

This uncertainty is pushing Gen Xers and late-stage Millennials to look for alternatives. For many, Bitcoin has become a surprising but serious contender.

Why Bitcoin Appeals to the 40+ Crowd

It’s easy to assume Bitcoin is a young person’s game, but that’s no longer the case. Recent surveys show that ownership and interest in cryptocurrency is rising fastest among Americans aged 40–60. Here’s why this demographic is warming up to Bitcoin:

Long-Term Appreciation Potential

Many people in their 40s and 50s missed the early crypto boom — but they’ve watched Bitcoin go from $300 to over $65,000 in less than a decade. Even if the biggest gains are behind us, Bitcoin’s finite supply and increasing institutional adoption make it attractive as a long-term hedge against inflation and currency debasement.

Distrust in Government and Financial Institutions

People over 40 have lived through multiple market crashes, bank bailouts, and political gridlock. Bitcoin offers a decentralized, non-governmental asset that can’t be printed or manipulated by central banks. That independence is a feature — not a bug.

Portability and Global Access

For those considering retiring abroad (a growing trend), Bitcoin is easily transferable, doesn’t require a local bank account, and can be accessed anywhere with an internet connection. It offers a level of flexibility traditional assets can’t.

Late-Stage Diversification

Many in this age group realize they won’t have enough saved in traditional accounts. Bitcoin offers a “catch-up” strategy for higher risk-tolerant individuals — with the potential for exponential growth, even over just 5–10 years.

Case Study: How Real People Over 40 Are Using Bitcoin in 2026

To put theory into perspective, here are a few real-life scenarios based on 2025–2026 trends and interviews from major financial media outlets:

🧔 Case 1: The Late-Saver Mid-Level Manager (Age 47)

Mike, a mid-level operations manager in Texas, had just $75,000 in his 401(k) by age 45. Realizing he was behind, he began allocating 10% of his monthly paycheck into Bitcoin via a cold wallet and 5% into a crypto IRA. He treats it like a long-term “moonshot” bet — but one backed by historical data.

“I’m not gambling. I’m just hedging against what the dollar might be worth in 15 years,” he says.

👩 Case 2: Divorced Single Mother Turned Side Hustler (Age 52)

Lisa, a teacher turned freelancer after a tough divorce, began earning crypto through online platforms and saving in Bitcoin as a form of digital emergency fund. She uses Strike and Cash App to automatically convert small USD earnings into BTC weekly.

Her goal isn’t massive wealth — it’s self-reliance and mobility. She says, “I don’t trust the pension system anymore. Bitcoin gives me control.”

👨🦳 Case 3: Retired Veteran (Age 59) Using Bitcoin as Legacy Planning

James, a retired veteran with a pension and no debt, uses Bitcoin not for income, but for legacy planning. He sees it as a long-term wealth transfer vehicle for his grandkids, storing it securely in a multisig wallet with estate instructions included.

“Gold is bulky. Real estate is complicated. Bitcoin is clean, borderless, and invisible,” he told a financial podcast in early 2026.

How Americans Over 40 Are Using Bitcoin for Retirement

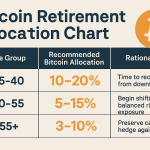

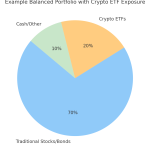

Contrary to stereotypes, most mid-life crypto investors aren’t going “all in.” They’re using Bitcoin in strategic, diversified ways, often allocating just 5%–15% of their total portfolio to digital assets. The key is not chasing overnight wealth but hedging against inflation, increasing upside exposure, and adding flexibility to traditional retirement plans.

Here are three common approaches:

- Buy and Hold (“Digital Gold” Strategy)

This is the most popular approach among older investors: allocate a small but growing share of your portfolio to Bitcoin, then hold long-term — often through at least one halving cycle (approximately four years).

- Many aim for 5%–10% of net assets in Bitcoin

- Rebalance annually or as life changes (inheritance, home sale, market crashes, etc.)

- Some also add Ethereum or a stablecoin like USDC for balance

This strategy mirrors gold investing — not for day-to-day income, but as a long-term store of value and hedge against fiat currency risk.

“I’m not trying to flip coins. I’m just trying to keep my future from being eaten by inflation,” said a 54-year-old Texan retiree in a recent Fidelity crypto survey.

- DCA + Profit-Taking (Moderate-Growth Strategy)

Dollar-cost averaging (DCA) is when you buy a set amount of Bitcoin regularly — weekly, bi-weekly, or monthly — regardless of price.

Many over-40 investors:

- DCA a small amount (e.g., $50–$300/month)

- Take partial profits during major bull runs (e.g., 20%–30% when BTC crosses $75K+)

- Reallocate those profits into safer retirement vehicles like TIPS, annuities, or I-Bonds

This creates a hybrid plan: ride the upside, then lock in safety as you approach retirement.

It’s especially popular for those with inconsistent income or late starts — like freelancers, immigrants, or self-employed individuals without a 401(k).

- Retirement Hedge / Escape Hatch Strategy

This is a more defensive play. Investors in their 40s and 50s use Bitcoin as:

- A geopolitical hedge (especially popular post-COVID and post-Ukraine war)

- A counterbalance to unstable currencies if retiring abroad

- A last-resort store of value in case the U.S. dollar falters in the next 10–15 years

Often, these investors:

- Use self-custody wallets (e.g., Ledger, Trezor)

- Don’t trade frequently

- Consider multi-generational BTC holdings (legacy planning)

For them, Bitcoin is not a retirement plan — it’s an insurance policy.

The Bottom Line: A Tool — Not a Savior

For people over 40, Bitcoin is not a magic solution. It doesn’t replace traditional planning, pensions, or social security. But it fills a critical gap:

- It’s an inflation-resistant store of value

- It can grow far faster than bonds or cash

- It’s borderless, private, and increasingly mainstream

In an age of uncertainty, de-dollarization, and distrust, Bitcoin gives retirement-age investors something they haven’t had in years — an asset they can control entirely.

The key is balance, education, and strategic positioning.

Mindset Shifts: Why Bitcoin Isn’t Just for the Young and Tech-Savvy

One of the most common misconceptions about Bitcoin is that it’s only for Gen Z or tech-obsessed Millennials. In reality, 2025–2026 data from Grayscale, Glassnode, and Fidelity show a notable uptick in BTC adoption among Gen X and Baby Boomers.

So, what’s changed?

Rebuilding Financial Confidence After Setbacks

Many over-40 investors are rethinking their strategies after:

- Divorce or career disruption

- Late-start saving or debt burdens

- Market crashes that wiped out previous gains

- Inflation eroding the real value of their savings

Bitcoin offers an alternative path to regain ground without depending on slow-growth vehicles like CDs or annuities.

“I was tired of being told it was too late. Bitcoin let me feel like I had options again,” said one 49-year-old investor in a CNBC interview in mid-2025.

Overcoming Fear Through Education

The volatility of Bitcoin understandably scares older investors. But those who spend time learning, even just an hour a week, tend to develop more realistic expectations and greater comfort with crypto.

Helpful strategies include:

- Following reputable educators like Lyn Alden, Preston Pysh, or Anthony Pompliano

- Using dollar-cost averaging to reduce fear of buying at the top

- Learning to self-custody using Ledger, Trezor, or multisig setups

- Joining retirement crypto communities (Reddit, Telegram, Clubhouse, even Facebook)

Knowledge reduces panic — and increases conviction.

Using Bitcoin as a Lifestyle Enhancer, Not a Retirement Savior

Finally, people over 40 are learning that Bitcoin doesn’t need to be their whole portfolio. Even a 5%–10% allocation, held long-term, has historically outperformed most traditional assets over 4–5 years.

It’s not about retiring rich overnight — it’s about:

- Diversifying your risk

- Increasing financial optionality

- Passing something meaningful to your children or grandchildren

This mindset shift — from “magic bullet” to “strategic tool” — is what makes Bitcoin realistic and emotionally sustainable for those in midlife.

Common Mistakes to Avoid When Using Bitcoin for Retirement After 40

While Bitcoin offers exciting potential, investors in their 40s, 50s, and beyond face a different risk profile than younger people. Your time horizon is shorter. Your margin for error is smaller. And your focus is shifting from growth to preservation.

Here are the most common mistakes older investors make when using Bitcoin for retirement — and how to avoid them:

- Going All-In Too Late

Some people discover Bitcoin at 48, see headlines about millionaires, and decide to bet the farm. But going “all in” on crypto close to retirement age is no different than betting your savings on one high-volatility stock.

Solution: Keep Bitcoin as a small slice of your portfolio — 5% to 15% at most. If your income is lower, scale it back to 2%–5%. Use it to diversify, not replace your entire plan.

- Not Understanding Self-Custody Risks

People over 40 often prefer traditional banking. But storing Bitcoin on exchanges (like Coinbase or Binance) carries risk. If the exchange gets hacked, goes bankrupt, or freezes withdrawals, your funds could be locked or lost.

Solution: Learn to use hardware wallets (like Ledger or Trezor). They give you full control of your crypto, similar to owning physical gold rather than a gold ETF.

- Chasing Gains With Meme Coins or Altcoins

Bitcoin has a track record. Many altcoins do not. Investors late to the game often try to make up for lost time by gambling on unproven coins, NFTs, or DeFi platforms. This often ends in losses or scams.

Solution: Stick to established assets — Bitcoin, Ethereum, maybe one or two others. If you’re not deeply experienced, skip the speculation.

- Having No Exit Strategy

Retirement investing isn’t just about buying — it’s about knowing when and how to exit. If BTC hits $150,000 in 2026, will you sell some? How much? What will you do with the profits?

Solution: Create a written plan:

- Sell X% if BTC hits $Y

- Move funds into annuities, TIPS, or dividend stocks

- Keep a long-term portion as generational wealth

Having a plan removes emotion when markets get volatile.

- Failing to Rebalance

Crypto bull runs can distort your portfolio. If Bitcoin jumps from 5% of your portfolio to 20%, your risk exposure rises without you even realizing it.

Solution: Rebalance once or twice per year. Trim crypto back to your target allocation and reinvest excess gains into lower-risk assets.

The Strategy?

Bitcoin can be a powerful tool for retirement after 40 — but only when treated as part of a broader strategy. Avoid these mistakes, stay educated, and you’ll be far more likely to enjoy the upside without sabotaging your long-term security.